All bank star-ratings have now been updated based on year-end 2024 data. (Credit unions will be out soon.)

The FDIC's new Acting Chairman, Travis Hill, (since January 20th) has already made two big changes in the release of new bank data: no more corresponding press conference and no more disclosing the assets of Problem Banks, just the number of banks that made the list.

Bauer's Troubled and Problematic Report currently contains 74 banks (1.66% of the industry), just slightly more than the FDIC's 66 (1.5% of the industry).

JRN by Bauer 42:09

All New Bank Star-Ratings Now Available

All bank star-ratings have now been updated, both on bauerfinancial.com and in Jumbo Rate News.

The FDIC has a new Acting Chairman, Travis Hill, (effective January 20th). Mr. Hill has already made two big changes in the release of new bank data. The first was to release the data without a corresponding press conference. From our experience, the press conference was basically just a reading of the findings, which are still available. The part we will miss is the Q&A session after the reading. For now at least, that is no more.

The other change is that the FDIC will no longer disclose the total assets of “Problem Banks”, only the number of banks on its “Problem List”. Based on 12/31/2024 data, there are 66 banks on the FDIC’s Problem List (1.5% of the industry).

Mr. Hill’s reasoning is three-fold. Disclosing the total assets of Problem Banks can lead to:

1) misidentifications;

2) Disorderly bank runs (his words: Bauer has yet to hear of an orderly bank run);

3) Supervisors may hesitate to downgrade a bank to troubled status if they feel it can be identified.

That’s okay. Bauer has its own “problem” list that comes pretty close to theirs. Bauer’s Troubled and Problematic Bank Report (all banks rated 2-Stars or below) currently contains 74 banks (1.66% of the industry). One of the largest additions to Bauer’s list is 2-Star UniBank, Lynnwood, WA (58407). Our reason for reporting this is also threefold:

1) Total assets at UniBank are $522 million but a leverage CR of just 5.60% makes it one of just six banks that ended 2024 less than “Well-Capitalized” by regulators.

2) UniBank posted quarterly losses in both the third and fourth quarter bringing its 2024 net income to –$31 million.

3) UniBank’s loan portfolio is 55% CRE. About 4.4% of those CRE loans are so delinquent they are no longer accruing interest. UniBank’s C&I loans, while a much smaller slice of the “loan pie”, are also showing weakness. Almost 19% of its C&I loans are now reported at some level of past due or delinquent.

The banking industry did have some positive news as well. Fourth quarter net income of $66.8 billion brought the full-year 2024 industry income up to $268.2 billion. That’s 5.6% higher than 2023. Net operating revenue was also up as both interest income and noninterest income improved from 2023.

- At year-end 2024, banking industry assets were up 1.8% from a year earlier while loans, the largest single component of assets, were up 2.2%.

- Domestic deposits were up 2.3% over the year and are now $4.5 billion (higher than before the pandemic). A large portion of this increase, however, is in estimated uninsured deposits, which increased 5.4%; insured deposits increased by just 0.5%.

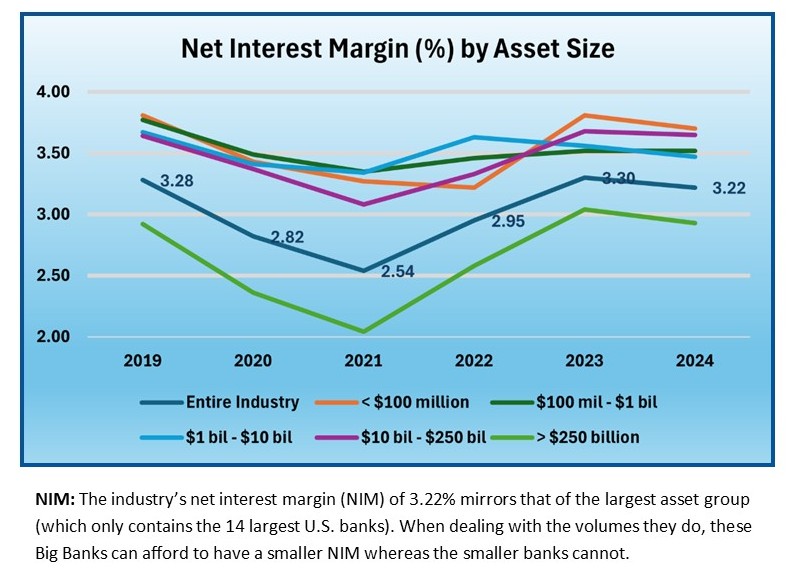

Finally, NIM is close to or above 3.5% for all asset size groups except the largest, which only contains 14 Big Banks. Net interest income increased by $5.4 billion as interest paid on deposits decreased by a greater amount than interest earned on loans. Noninterest income was aided by higher trading revenue and income from fiduciary activities, which added another $9.8 billion. That comes to a gain of $15.2 billion (6.3%) in net operating revenue.

Only three current JRN listees changed categories as a result of the new star-ratings release. They were:

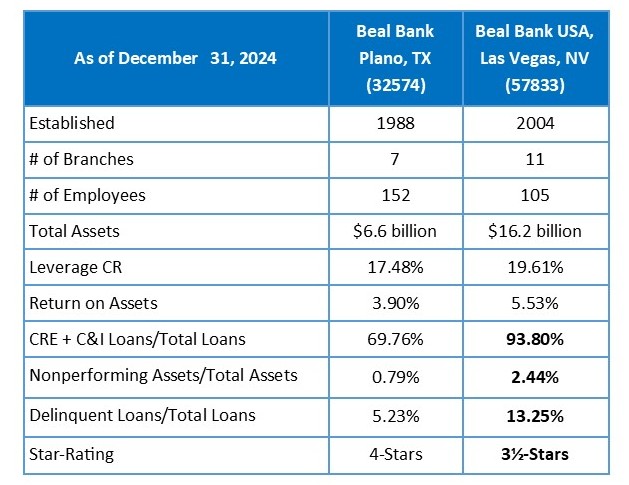

4-Star Beal Bank, Plano, TX (32574) was upgraded from 3½-Stars. The same cannot be said for its affiliate, JRN listee 3½-Star Beal Bank USA, Las Vegas, NV, (57833) (which we wrote about in JRN 42:07 Problems Persist in Commercial Loans).

Both Beal Banks are heavily invested in commercial loans, but with nearly 94%, Beal Bank USA almost excludes all other types of loans. The quality of the loans at Beal Bank USA is somewhat less than stellar as well. The following is a comparison of the two affiliates at year-end 2024.

The other two listee Star-Rating changes were both downgrades. First Internet Bank of Indiana, Fishers, IN (34607) witnessed a drop in its leverage capital ratio (to 8.23%) that resulted in the loss of a star. It was downgraded from 5-Stars to 4-Stars.

3½-Star Greenville Federal, Greenville, OH (27965) also saw a drop in its leverage capital ratio, but to 7.95%. Greenville Federal is a typical thrift, with over 64% of its loans going into residential real estate. The quality of its loan portfolio is quite good. However, Greenville Federal posted four consecutive quarterly losses in 2024. A combination of the low leverage CR (< 8%) and the losses, dropped Greenville Federal from a recommended rating to 3½-Stars.