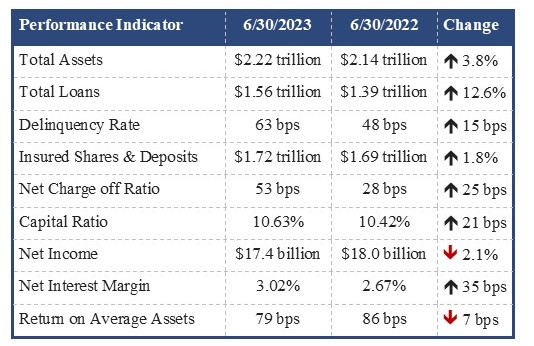

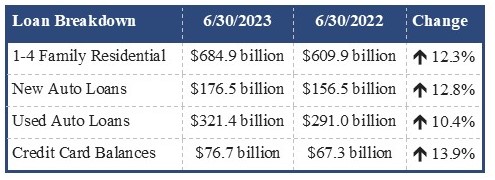

Credit Unions posted double digit increases in all major loan categories over the 12 month period ending June 30, 2023. However, delinquencies and charge-offs are also on the rise.

So, much like we reported with banks last week, the 51 credit unions listed on page 5 of this week’s Jumbo Rate News are on our watch list for nonperforming loans.

Those with a star-rating of 2-Stars or lower can be found on Bauer’s Troubled & Problematic C.U. Report.

All New Credit Union Star-Ratings Available

All credit union star ratings are now updated based on June 30, 2023 financial data. Last quarter we focused primarily on loan growth (up 17.6% from a year earlier). We also noted that the percent of nonperforming loans was climbing as well. Both are still growing, but as loan growth has decelerated the percent of nonperforming loan growth is accelerating.

So, much like we reported with banks last week, the 51 credit unions listed on page 5 of this week’s JRN are on our watch list for nonperforming loans. In addition to being rated 3-Stars or lower, each credit union has high delinquencies (represented by a nonperforming asset ratio of at least 2.7% AND loan loss reserves sufficient to cover less than 80% of those nonperformers).

An additional 31 federally-insured credit unions would also fall into this category, except that they are too small to be rated by Bauer (i.e. they have less than $1.5 million in assets). So, for example, four credit unions have negative Bauer’s Adjusted capital ratios (CRs). Only two of them are listed on page 5 because the other two have less than $1.5 million in assets.

The two that are listed are:

1-Star Bykota FCU, Brooklyn, NY, which has assets if $2.1 million, and 2-Star Star City FCU, Roanoke, VA (with assets of $2.5 million).

Bykota FCU is a faith-based credit union that was established in 1970. It has fewer than 1,000 members. Its loan volume has actually been declining over the past year (from $687,000 to $567,000 or about 17½%). Its delinquencies, while travelling at roughly the same rate, are heading in the opposite direction—up instead of down.

While Bykota’s pace is gradual, Star City FCU dropped from a 4-Star rating to 2-Stars in a single quarter. Star City FCU’s delinquent loans (which were zero a year ago) jumped over 500%-from $37,000 up to $246,000 during the 2nd quarter.

Its delinquency to asset ratio went from 1.5% to 10% in that single quarter and its Bauer’s adjusted CR dropped from 8.55% to below zero. Star City FCU may report higher assets than Bykota FCU, but it has about a third fewer members (581 at 6/30/2023). It has 277 loans on its books (just shy of $2 million worth). About one-third of that total loan amount is unsecured.

The two C.U.s that are too small to rate are: U.S. Employees FCU, Fairmont, WV and New Pilgrim FCU, Birmingham, AL.

With assets of just $745,000 and only 133 members, U.S. EFCU only has 38 loans on its books. At June 30th, ten of those loans were at least 60 days in arrears.

New Pilgrim FCU has other problems besides troubled loans. With a capital ratio of just 2.64%, it is significantly undercapitalized by anyone’s standards. In addition, almost 20% of its loan portfolio is delinquent. That puts its Bauer’s Adjusted CR down to -3.65%. It’s a good thing New Pilgrim has a faith-based field of membership; its 550 members will need all the help they can get to dig out of this hole.

Two other credit unions are significantly undercapitalized with June 30th data. Both are in the state of New York and both are rated Zero-Stars. They are: Concord FCU, Brooklyn and Branch 6000 NALC CU, Amityville.

As for the industry as a whole:

As has been the case for several years now, the largest credit unions, those with assets of at least $1 billion, show the strongest growth in assets, membership and net worth. There are now 421 credit union in this category (up from 412 a year ago). These 421 credit unions hold 76% of total industry assets.

Over the past year, membership in the 421 largest credit unions grew 6.2%. Membership dropped in all other assets size categories.

The number of federally-insured credit unions continues to decline. During the twelve months ending June 30, 2023, we lost 167 credit unions (from 4,853 to 4,686). The number of credit unions with low-income designations also declined—from 2,620 a year ago to 2,585 today. The percentage of those CUs earning Bauer’s top 5-Star rating dropped from 57.1% in Q1’23 to 56.7% in Q2. There are 115 institutions on Bauer’s Troubled & Problematic C.U. Report.