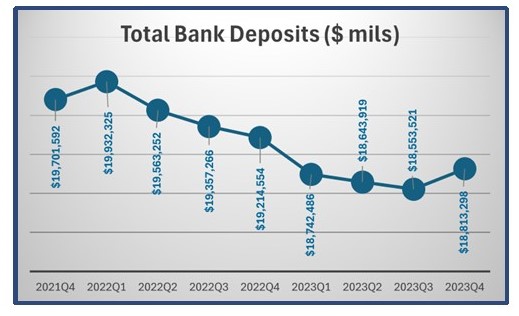

During the fourth quarter 2023, for the first time in seven quarters, domestic deposits at our nation's banks grew.

That growth appears to be the direct result of increased interest being paid by these banks.

It pays to do your homework, though. By using Jumbo Rate News (or our CD Rate Watch page for consumers), you can earn as much as $2,470 more in interest on a 1-year CD. And, of course, the more CDs you have, the more you stand to gain.

Bank Deposits Gain Interest, in More Ways than One

Let’s start by stating the obvious. One of the primary businesses of a depository institution is to grow deposits. That may seem to go without saying yet, during the 12 months ending December 31, 2023, 45% of the nation’s banks did the opposite; they lost deposits.

In fact, during the fourth quarter, domestic deposits increased for the first time in seven straight quarters, with time deposits (CDs) leading the way. That one quarter increase did not help the year-to-date totals much. At Dec. 31st, total deposits were still down 2.1% over the year.

At community banks, however, total deposits have increased for two consecutive quarters and 60% witnessed an increase from third quarter numbers.

Of course, that was helped by the Federal Reserve’s 11 interest rate increases in two years. They brought the Fed Funds rate from near zero to over 5.25%. CD rates followed, eventually. People are suddenly interested in the CD market again.

FUN FACT:

The average CD rate at the end of 2022, was 0.88%.

One year later, that average was up to 2.93%.

The top 1 year CD rate in Jumbo Rate News: 5.40%

The average CD on banks’ collective books was costing banks (and earning customers) 0.88% at the end of 2022. That includes all CDs, whether they were purchased when rates were at historic lows or purchased recently at higher rates.

By the close of 2023, that average had more than tripled to 2.93%. Again, that’s the average bank cost of all CDs on their books. As JRN readers, you know very well that you can get a much better rate today than 2.93%. Our top 1 year CD rate has been hovering between 5.40% and 5.50% all year thus far.

Let’s do the math:

A $100,000 CD at 2.93% APY will yield $2,930 over the course of the year, or $244.16 per month, if you elect monthly interest payments.

A $100,000 CD at 5.40% APY will yield $5,400 over the course of the year, or $450 per month, if monthly interest payments are requested.

That’s an extra of $2,470 in your pocket on one, one-year CD, just by using Jumbo Rate News (or our CD Rate Watch page for consumers). The more CDs you have, the more you stand to gain.

You do have to be on your toes, however. If you miss the maturity date, most CDs will automatically rollover at a significantly lower rate. A recent Wall Street Journal article cited a rollover rate of just 0.05%. The owner missed the grace period to move the CD without penalty.

At this point, the choices are pay an early withdrawal penalty or accept the new rate. In the case of a 0.05% rate, accepting the penalty is likely the better choice. Even if the penalty is 12 months of interest, it only amounts to $50.

There are 50 banks listed on page 5 of this week's Jumbo Rate News. They are all community banks (by the FDIC definition at least) and are currently rated either 5-Stars or 4-Stars by Bauer. Each reported 2023 deposit growth of over 37%.

Not all growth was organic, as you can imagine. Mergers and acquisitions play a part in much of the growth we see today. That was the case at the $111 million asset 5-Star Maynard SB, IA, which had just $72 million in assets at the end of the third quarter 2023. Its parent, Fayette Bancorp made the decision last year to merge its two affiliate banks together. On November 3, 2023, the smaller Citizens SB, Hawkeye, IA, with its $31 million in assets, was merged into Maynard SB.

The stated purpose of the merger was to allow the banks to provide more services to their customers, including expanded lending. That makes sense to us as Maynard SB has a loan to deposit ratio of just 48%, well below the 74% of its peer group. It’s time to put those deposits to work.

There are also some relatively new banks on this list. 4-Star Bank Irvine, CA, for example, was established in October 2022. Strong growth is expected in the early years of a bank and Bank Irvine has not disappointed. Its assets grew 409% during 2023 and loans grew by 1061%, but it was deposits that had the strongest growth at 1666%.

Created to provide personal and business services to a predominantly minority Orange County, Bank Irvine was organized by a group of community bankers and other professionals from the Chinese community in Southern California. It’s tagline is: Chinese culture, American Standard makes Bank Irvine your hometown bank!

Another shameless plug for community banks? Yes, but we don’t care. We love community banks because community banks love their communities. It’s really that simple.