Nearly 80% of U.S. banks reported increases in total deposits. A similar percentage of banks reported increases in interest-bearing deposits but the same cannot be said for non-interest-bearing, or core, deposits.

Today, the average net interest margin at our nation’s banks is at a comfortable 3.25% (annualized), but this shift in deposits will increase the interest banks pay. Without a corresponding increase in interest earned, this margin is apt to get squeezed again.

At March 31, 2021 (four years ago), the average bank net interest margin was just 2.54%, its lowest level on record. We do not want to return to that.

Bank Deposits Migrate into Interest-Bearing Accounts

March 31, 2025 bank data revealed that domestic deposits at U.S. banks have risen for the third consecutive quarter. Deposits were up $180.9 billion (or 1%) from year-end 2024 and 2.2% from a year ago. Nearly 80% of U.S. banks reported increases in total deposits.

Similarly, 79% of banks reported increases in interest-bearing deposits whereas only 57% reported increases in non-interest-bearing deposits. We actually began noticing this migration from non-interest-bearing deposits to interest-bearing deposits in 2022 (JRN 40:07).

That’s not surprising since 2022 is when the Federal Reserve raised the Fed Funds rate from near zero to between 4.25% & 4.50%. Rates rose another percentage point before the end of July 2023 and even though that last gain was wiped-out in 2024, savings and CD rates are still much more attractive than they had been in a long time (since 2007).

The 50 banks on page 5 each grew total deposits by a minimum of 1.25% during the 12 month period ending March 31, 2025. In each case, interest-bearing deposits increased robustly while noninterest-bearing deposits decreased. In addition, each of these banks was established prior to 2020 and has total assets exceeding $150 million.

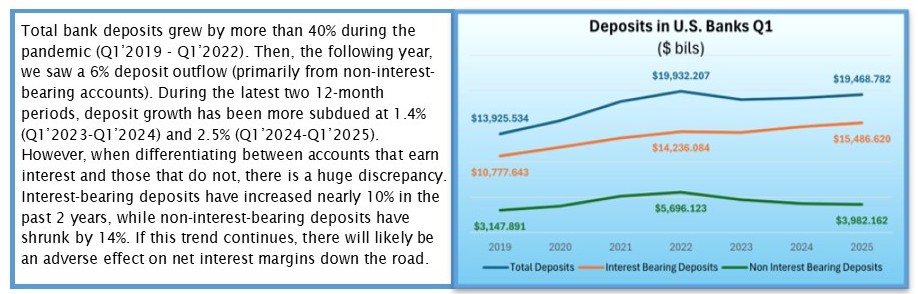

According to the call report data, after increasing 5.9% a year earlier, interest-bearing deposits increased another 3.7% during the 12 months ended March 31, 2025. Conversely, non-interest-bearing deposits have been on the decline, decreasing for three consecutive 12 month periods, and registering a total loss of more than 30% since March 31, 2022.

Bankers love non-interest-bearing accounts: they do not incur any interest expense, nor do they incur the same scrutiny as things like “brokered” deposits, which can be considered “hot” money. Non-interest-bearing, or core deposits, are basically a free loan for the bank. Not only do bankers love them, so do their regulators.

Other accounts, like savings and CDs, do incur interest expense. And while CDs, in particular, are committed for a specific length of time, these deposits are often placed by those chasing higher yields (like JRN subscribers). As non-core deposits, there is no real expectation of a long-term bank-depositor relationship.

Nonetheless, these deposits will typically be used to make loans at a higher percentage rate than what they are earning. This net interest margin (the difference between what the bank pays for deposits and the interest it earns on loans and other earning assets), is a critical measure.

Four years ago, March 31, 2021, the average net interest margin at our nation’s banks had contracted to 2.54%, its lowest level on record. Today, it is at a comfortable 3.25% (annualized), but is that sustainable?

Of the banks listed on page 5, 5-Star Seymour Bank, Seymour, MO (15701) reported the highest growth in interest-bearing deposits (over 214%). Seymour Bank had a history of taking an occasional brokered CD, but in first quarter 2024, it increased its reliance on brokered deposits. Brokered deposits went from accounting for less than 1% of total deposits to over 8% in just a few quarters. At March 31, 2025, its brokered deposits of $11.534 million were down from year-end 2024, when it reported $16.572 million in brokered deposits.

Brokered deposits, as a rule, require higher interest rates than other deposits. This can be a high price to pay to maintain a bank’s deposit base. Total deposits at Seymour Bank were up less than 5% over the year.

Another that has turned to brokered deposits is 4-Star Loyal Trust Bank, Johns Creek, GA (59182). Loyal Trust Bank began with $6 million in brokered deposits in the second quarter of 2023, by the end of that year, brokered deposits were up to almost $16 million (12% of total deposits). Today they are up to nearly $30 million, or 19% of total deposits. In spite of this, twice (Q3’2023 and Q4’2024) its loan to deposit ratio has exceeded 100%.

Loyal Trust Bank currently has a net interest margin of just 2.51%. Not only is that well below its peer group average of 3.67%, it places Loyal Trust Bank in the 7th percentile among its peers. Compare that to year-end 2023 when it was in the 53rd percentile. That’s not the direction we want to see.