June 30th financial data has now been evaluated for all federally-insured banks and credit unions. New star-ratings and reports can be found at bauerfinancial.com.

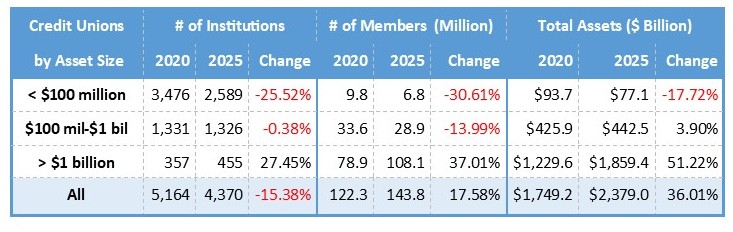

During the five years ended June 30, 2025, the number of credit unions with assets under $100 million has been cut more than 25%, membership at these smaller institutions has dropped over 30%, and total assets by nearly 18%.

Conversely, the group with assets exceeding $1 billion reported robust growth on all fronts. We have the 50 credit unions that grew their assets by the highest percentage rates listed on page 5 of this week's issue of Jumbo Rate News. They have used different methods to grow, and the results may not be as pretty as they had hoped for.

Credit Union Ratings are Now Updated

June 30th financial data has now been evaluated for all federally-insured banks and credit unions. New star-ratings and reports can be found at bauerfinancial.com.

Based on this new data, there are now just 82 credit unions listed on Bauer’s Troubled and Problematic Credit Union Report (rated 2-Stars or below and/or undercapitalized). That represents just 1.9% of the industry’s credit unions and less than 0.5% of total industry assets.

That’s great news. Less great is that small credit unions are much more likely to be found on this dubious list than their larger counterparts. Of the 82 credit unions currently on the list, 67 (82%) have less than $100 million in assets. Only two have assets greater than $1 billion, but that is a much smaller pool.

How long it will be this way is anyone’s guess. The larger credit unions keep getting bigger as the smaller ones diminish. During the five years ended June 30, 2025, the number of credit unions with assets under $100 million has been cut more than 25% (see chart below), membership at these smaller institutions has dropped over 30%, and total assets by nearly 18%.

Conversely, the group with assets exceeding $1 billion reported robust growth on all fronts. The 50 credit unions listed on page 5 each grew their assets by a minimum of 22.5% during the 12 months ended June 30, 2025. Only five have assets greater than $1 billion. (To make the list more meaningful to a wider range of readers, we eliminated all institutions that are less than 10 years old as well as those with total assets less than $5 million.)

The question is, how did they grow? 3-Star Pima FCU, Tucson, AZ (7316) was one of several credit unions that recently completed the purchase of a bank. On May 3, 2025, Pima FCU acquired Republic Bank of Arizona, Phoenix, AZ, a $284 million asset community bank.

It was not a big bank, but when combined with Pima’s organic growth, the addition of Republic Bank was enough to propel Pima from $1.237 billion in assets to $1.533 billion. The transaction came at a cost, though, as Pima FCU is now just “Adequately Capitalized”.

Credit unions buying banks has become much more common in recent years, but it still is much less common than credit unions buying other credit unions. In July 2024 5-Star River Region Community Federal Credit Union, Jefferson City, MO (24955) purchased Multipli Credit Union, Springfield, MO, a $184.261 million asset credit union. Then, in April 2025, it acquired Missouri Credit Union, Columbia, MO.

The two transactions boosted River Region’s assets from $522.012 million to $1.364 billion—a 161% jump. That’s a lot to digest. Yet, River Region Community FCU is still “Well-Capitalized by regulators, and still 5-Star rated by Bauer.

5-Star Mutual Federal Credit Union, Vicksburg, MS (24948) is another that acquired two credit unions during the 12 month period. The first was Mississippi FCU, Jackson, MS, a $161.6 million asset credit union, last October. Then, in April, it acquired insolvent JPFCU Federal Credit Union, a tiny ($0.406 million asset) credit union with one employee and 152 members.

It was the former (not the latter) that secured a position on page 5 for Mutual FCU. Its asset size grew from $310.828 million to $486.97 million—a 56.67% increase.

3-Star Local 265 IBEW Federal Credit Union, Lincoln, NE (15522) has not acquired another institution—bank or credit union. Yet, it managed to grow its assets organically by 47%. (Sometimes it helps to be small; it is the smallest on page 5.) Local 265 IBEW FCU grew from $3.707 million in assets to $5.463 million over the 12-month period. Its membership also increased from 988 to 1,402. Like, Pima FCU (on page 1), this growth resulted in Local 265 IBEW FCU’s regulatory capital classification dropping below the “Well-Capitalized” designation. Both of the credit unions are now “Adequately Capitalized”. (To put that in perspective, only 63 of the nation’s federally-insured C.U.s are currently less than well-capitalized.)

The C.U. industry reported an increase in total assets of $82 billion (3.6%) over the year. Loans, the largest piece of the asset pie, grew 3.9% ($64 billion). Credit union membership growth has been slow but steady; the industry added 2.8 million members during the same 12-month period, an increase of 2%.

The delinquency rate is something we are monitoring. As we reported two weeks ago (JRN 42:33), the delinquency rate is still below 1% (0.91%) but it has been climbing steadily since 2021. At June 30, 2021 the credit union delinquency rate was just 0.46%.