As we write this week’s article, CEOs of six of the nation’s largest banks are taking a verbal beating from Congress. Lawmakers took exception to some of the ways they perceive these bankers have taken advantage of poorer clients during the pandemic. Overdraft fees took the lead, and with good reason.

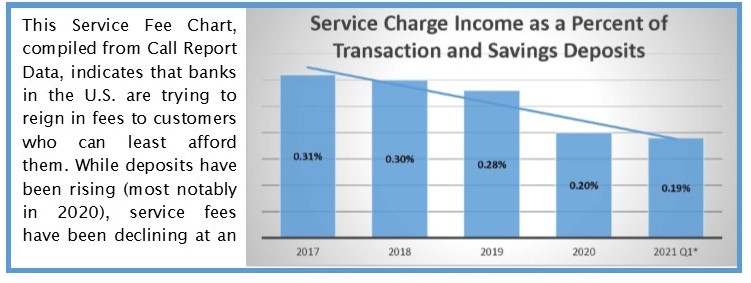

While “most” community banks were working very hard to get their neighbors and friends through the roughest months of the pandemic, the same cannot be said for some of their larger counterparts. As a matter of fact, it cannot even be said of “all” community banks as over 400 community banks had more than twice the industry average of service charge income as a percent of transaction and savings deposits (0.20%) in 2020.

But Big Banks, with trillions of dollars in assets and almost as much in deposits, should be able to charge less per transaction and still make a significant amount of money. Of the bankers getting the tongue-lashing though, only one, Jane Fraser of Citigroup, can say her bank has really reigned these charges in.

In 2019, the percent of service fees to transaction and savings deposits was 0.10%, much lower than the industry average of 0.28%. It was even lower in 2020 at 0.09%. Compare that with 0.38% in 2019 for Bank of America and 0.41% for Wells Fargo. Bank of America has reportedly stopped charging fees on debit card transactions so in 2020 its ratio went down to 0.27%. Wells Fargo’s was still at 0.32% in 2020.

So while there is still much work to be done to lower service fees, there has been progress that deserves to be recognized. That brings us to another area that has the attention of regulators, lawmakers and community groups: modernizing the 1977 Community Reinvestment Act (CRA). Most Big Banks have Satisfactory or Outstanding CRA ratings, but these CEOs provide valuable input on the subject. The only Big Bank that Needs to Improve its CRA rating is 4-Star USAA FSB, San Antonio, TX. You can find it on page 7 along with all others rated Needs to Improve (NI) or Substantial Noncompliance (SN).

Only two banks are currently rated SN: 4-Star Evolve Bank & Trust, West Memphis, AR and 3-Sar Lemont National Bank, IL. Although two others with SN ratings were among the 25 banks that were lost to merger in the first quarter (JRN 35:21): Bank of Hamilton, ND and Reynolds State Bank, IL were both acquired in February.

This is a topic that was at the forefront before the pandemic and is resurfacing now that life is beginning to get back to “normal”. The COVID-19 pandemic has underscored the need to modernize CRA. As Federal Reserve Chairman, Jerome Powell noted in remarks: made last month at the “2021 Just Economy Conference”,

“The economic downturn has not fallen evenly on all Americans, and those least able to bear the burden have been hit the hardest.” He went on to cite statistics from an upcoming report that reveal 22% of parents nationwide were unable to work regular hours due to disruptions in childcare and school. That number grows to 30% for Hispanic and 36% for Black mothers, as these groups were disproportionately affected."

The Office of the Comptroller of the Currency’s (OCC) newly appointed Acting Comptroller, Michael Hsu, has also noted the urgency of updating CRA. As an interim leader, Hsu does not want to make any changes that can wait for a confirmed comptroller. CRA, however, is not in that category. In fact, it has become a top priority. Hsu, like Powell, sees the disparity in the pandemic and the recovery when it comes to minorities and low-income people.

Hsu’s predecessor, Joseph Otting, already had CRA changes in the works, but they are on hold until Hsu’s team has time to deliberate. The OCC could decide, as it did under Otting, to go it alone, or it could collaborate with the Federal Reserve and FDIC. Theoretically, three agencies should be able to come up with better solutions than one.