Fourth‑quarter 2025 Bauer star ratings for all federally insured credit unions are now available.

The share of recommended credit unions (5-Stars or 4-Stars) slipped from 86% to 84%, while the share rated 2‑Stars or below also declined—leaving more institutions in the “adequate” middle tier.

The industry remains broadly stable, but rising delinquencies and pockets of severe underperformance—especially among smaller institutions—underscore the importance of strong underwriting and regularly checking Bauer star ratings.

Jumbo Rate News JRN 43:11

New Credit Union Star Ratings and Data Now Available

Star-Ratings based on fourth quarter 2025 financial data are now available for all federally insured credit unions as well as banks (released two weeks ago).

The percent of C.U.s recommended by Bauer (i.e. rated 5 or 4-Stars) dropped from 86% to 84% of the industry during the fourth quarter. The percent on Bauer’s Troubled and Problematic Credit Union Report (i.e. rated 2-Stars or below) also decreased during the quarter. That leaves a higher portion right in the middle—solidly Adequate.

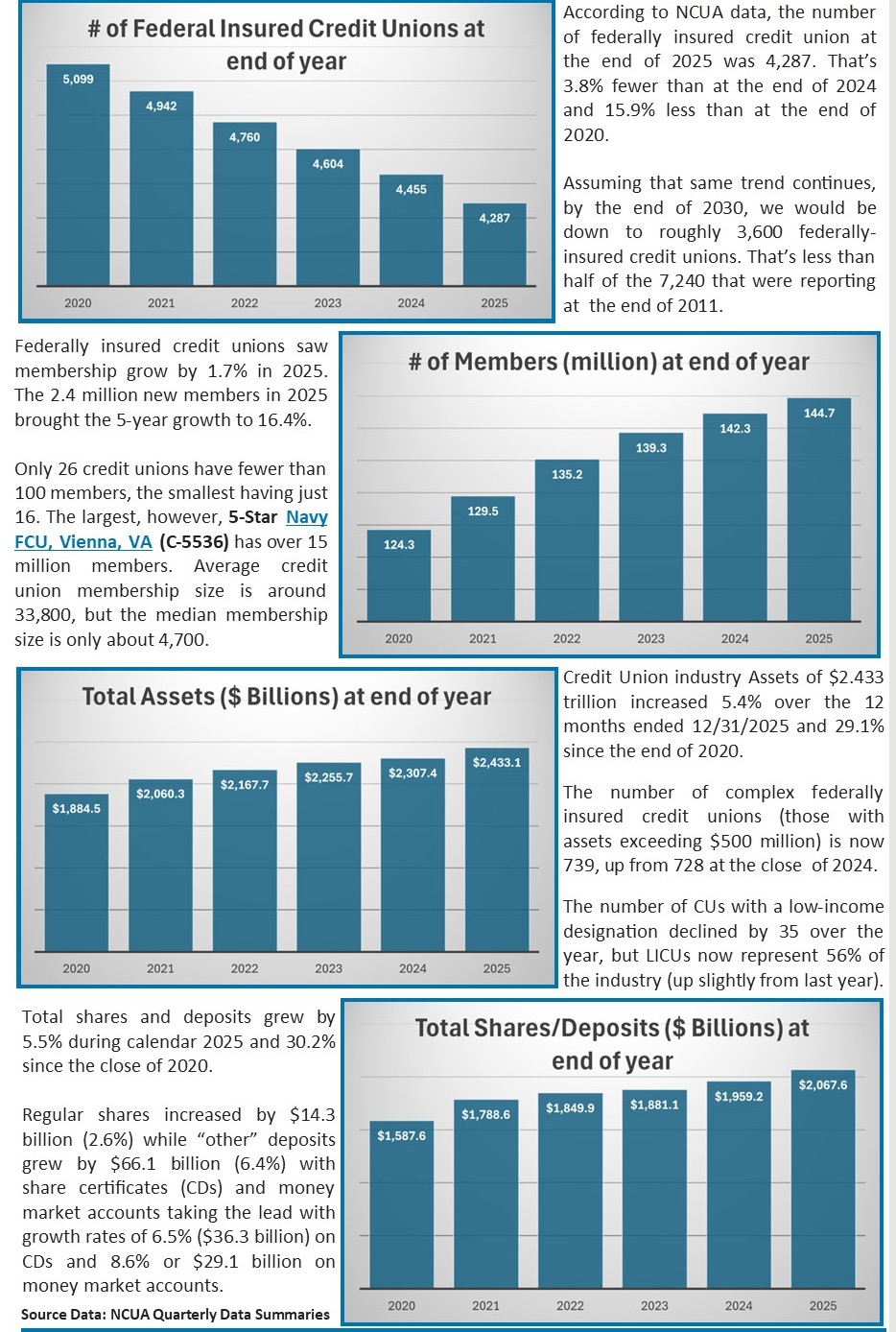

Credit union industry assets grew 5.4% or $125.7 billion, during calendar 2025, ending the year at $2.43 trillion. Over 60% of that growth was in the form of loans, which we want to take a closer look at - loan quality, to be more precise.

According to NCUA data, the delinquency rate for the industry is 103 basis points, which is five basis points higher than a year earlier. Almost 1,500 credit unions have a delinquency ratio exceeding that 1.03%. Several hit double digits.

Zero-Star Sixth Avenue Baptist FCU, Birmingham, AL (15938), for example, has a nonperforming asset ratio of 10.37%. It’s a small CU with total assets of just $5.218 million and it has fewer than 850 members.

While its specific story may be of interest to only a small fraction of the population, it is a prime example of the importance of underwriting.

Over half of Sixth Avenue Baptist’s loans are secured by automobiles, mostly used, and another 20% is in the form of single-family mortgage loans. Nearly 96% of its delinquent loans come from these loans (one new vehicle, four used vehicles and two single family homes are 60 days or more in arrears).

Unsecured loans make up the other 4% of delinquent loans (three payday alternative loans and six other unsecured loans or lines of credit).

It drives the point home that small institutions, in particular, must be steadfast in their underwriting. Sixth Avenue Baptist has a total of 217 loans on its books. Of those, 16 are delinquent. That represents 7.3% by number and 14.6% by dollar amount, and we are not seeing much improvement.

In fact, this marks the third consecutive quarter that Sixth Avenue Baptist has reported both a negative Bauer’s Adjusted Capital Ratio (CR) (currently -1.5%) and a Texas Ratio exceeding 100% (currently 107.34%).

Larger institutions are not immune to bad loans. For example, this is the second quarter in a row in which 1-Star Civic Federal Credit Union, Raliegh, NC (24003) has reported a nonperforming ratio over 6%. With a Bauer’s Adjusted CR of just 0.26% and a Texas Ratio near 80%, its loans are not in quite as bad a shape as Sixth Avenue Baptist, but it has other issues as well.

Civic FCU has only posted one profit in the last 13 quarters. Its loss for 2025 was $123.7 million—more than half of its remaining $235.497 million net worth. If anything were to happen to Civic FCU, the fallout would reach a lot more of the population. Total assets at this credit union exceed $3.3 billion and it has more than 350,000 members.

However, Civic FCU is a Certified Community Development Financial Institution (CDFI) by the U.S. Treasury Department. As such, it is committed to financial inclusion and serving members who lack access to loans, equity investments, and/or financial services. It also has resources available that others do not (e.g. CDFI capital and technical assistance grants, to help it meet the needs of the community).

CDFIs may provide flexible loan underwriting and specialized products for small businesses and affordable housing. The priority is generating economic growth and opportunity in distressed areas. That being the case, we expect a concerted effort to re-work faltering loans (much more so than at a non-CDFI).

Civic FCU reported $260 million in uninsured shares and deposits (representing 9.4% of the total) at the end of 2025. That’s high, but it is far from the highest. The highest amount, by far, is the $15.948 billion that 5-Star Navy FCU, Vienna, VA (5536) has in uninsured deposits. Navy FCU is rated 5-Stars and it dwarfs all other C.U.s in every size measure.

Conversely, Zero-Star North Bay Credit Union, Santa Rosa, CA (63373) is undercapitalized with a regulatory CR of 4.69%. It has not posted a profit in the last 10 quarters. Its nonperforming asset ratio of 2.87% was down from 3.72% last quarter. Its Bauer’s Adjusted CR is just 1.87% and its Texas Ratio is 49%. But the kicker is, at over $48 million, its uninsured shares and deposits are over 52% of total shares and deposits.

Fortunately for North Bay’s members, it does not have to worry about that. On March 1, 2026, North Bay C.U. was merged into 5-Star Corporate America Family Credit Union, Elgin, IL (68215). Corporate America Family CU was established in 1976 and has since acquired dozens of other C.U.s. This marks its first such transaction since May 2020 and its first outside of Illinois since 2004.

As an industry, federally insured credit unions reported more than $206 billion in uninsured shares and deposits. While many of those deposits are at highly rated credit unions, like Navy FCU, many are also at subpar institutions. We can’t stress enough the importance of checking Star-Ratings quarterly.