All star-ratings (banks and credit unions) have now been updated based on September 30, 2024 financial data.

Two items really stood out in the new credit union data: a rise in delinquencies and charge-offs as well as an indication that borrowers are tapping into existing credit lines rather than seeking new loans.

This week we also revisited brokered deposits and whether there is any connection between them and the big bank failures of 2023.

JRN by Bauer 41:48

New Credit Union Star Ratings and Data Now Available

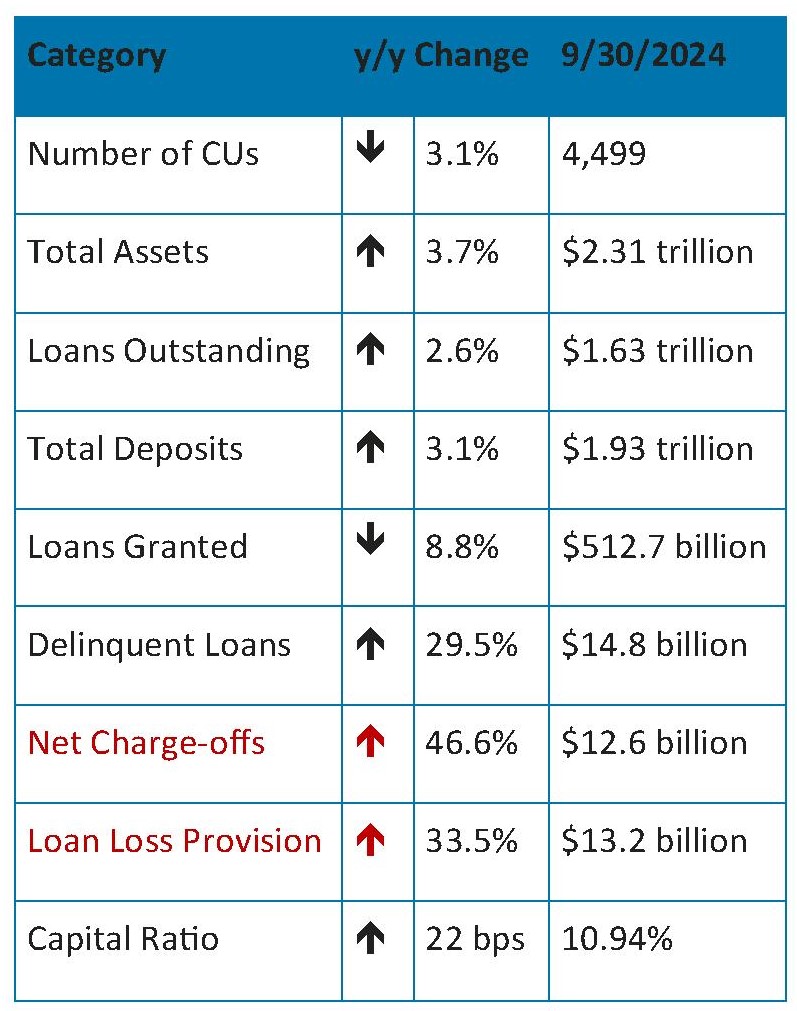

All star-ratings (banks and credit unions) have now been updated based on September 30, 2024 financial data. Third quarter credit union data, we discovered, showed a mixed bag of results.

In the last four quarters, 145 federally-insured credit unions have been lost, primarily due to mergers. Of those, 128 had low-income or (LICU) designations. Roughly 54.4% of federally-insured credit unions now carry the LICU designation. That’s slightly below the 55.4% reported a year ago.

Also, over the last 12 months:

A 3.1% drop in the number of credit unions is consistent with what has been happening over the last several years. However, there are two items that do stand out in this chart. The first is that delinquent loans and charge-offs are rapidly rising. That’s not good. Fortunately, loan loss provisions are rising as well.

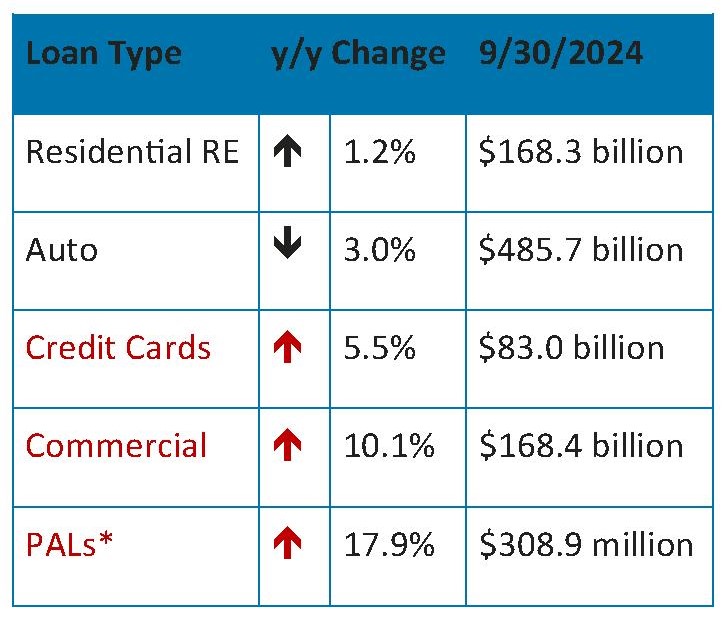

The second thing we noticed is that while total loans outstanding grew 2.6% over the course of the year, new loans granted dropped 8.8%. That could indicate that borrowers are pulling from previously granted lines of credit. Here’s a breakdown:

*PALs, or Payday Alternative Loans, are short term loans offered only by federal credit unions. They may be granted in amounts up to $2,000.

Since 2019, the number of PALs issued has been on the rise. That, however, was by design. In 2019, the rules governing these PALs changed. It was an effort to drive credit union members to their credit union for emergency cash, and away from more expensive and possibly predatory, alternatives (JRN 36:37).

Five years later, it is impossible to discern how much of this growth is still because of that 2019 rule change and how much is due to increased demand. A 5½% increase in credit card balances leads us to believe that each may play a part.

Brokered Deposits: a Source of Liquidity or Risk?

Speaking of 2019... We ran a three-part series in 2019 chronicling brokered bank deposits from the 1980s to new rules that were being drafted at that time. Brokered deposits were demonized after the savings and loan crisis of the 1980s. Bauer was perhaps the first to see the writing on the wall (JRN 36:16, :17 , :18).

The first bank to fail as a result of brokered deposits, was Penn Square Bank of Oklahoma City, OK in1982. Penn Square had used brokers to bring in deposits it then used to make speculative gas and oil exploration loans. This was just the beginning. Hundreds of banks and S&Ls suffered similar fates before Congress finally passed the Financial Institutions Reform, Recovery and Enforcement Act of 1989 (FIRREA).

As is often the case, some things were overlooked when FIRREA was drafted and adopted. On April 1, 2021, new rules closed a loophole that had enabled “less than Well-Capitalized” banks (and savings and loans) to accept brokered deposits without restrictions. While most banks were (and are) “Well-Capitalized”, these new procedures kept banks from using brokers to bring in emergency, high-cost deposits, in the event they fell below that threshold (JRN 38:13). This new rule also redefined the term “broker”, which eliminated several areas of confusion that surrounded the FIRREA rules.

Over the years, we discovered brokers were not the only problem. Nor was it all brokers that posed a threat to the system. There was a subset of unscrupulous brokers that had no regard for the condition of the bank when they placed funds for their clients. They were not acting as fiduciaries, whose responsibility it is to look out for the best interest of their client. They acted in their own best interest. The highest commission won the deposits.

Brokers did not act alone, however. There were also bankers who decided to speculate with federally-insured deposits. In most cases, desperation drove them down this path. The bank was in trouble and the officers were grabbing at straws to turn things around. The combination of FIRREA and this addendum stopped these bad actors in their tracks.

When 2023 brought more (and Big) bank failures, some had an ill-conceived idea to make brokers and brokered deposits the scapegoat. Silicon Valley Bank, the first to fall, had no brokered deposits when it failed.

That being said, if not managed properly, too much reliance on brokered deposits can still become a problem. Brokered deposits represent at least 35% of total deposits on all banks listed on page 5. These banks are all “Well-Capitalized”, but their Bauer star-ratings vary based on their overall financial picture.

1 comment on “New Credit Union Star Ratings and Data Now Available”

Comments are closed.