U.S. banks are engaged in a continuing effort to replenish reserves that had been allowed to drop by more than 18% after the pandemic shutdown.

In the past two years, total loans at U.S. banks increased 9.3%; loans to consumers grew slightly more at 10.8%. However, unsecured credit card loans grew more than 27%. The percent of those unsecured credit card loans that are falling behind is just as troubling.

Pumping Up Reserves for Potential Loan Losses

A bank increasing its loan loss reserves is a pretty good indication that it expects to be hitting some turbulence in the loan “pay back” department. Similar to a pilot, it prepares for rough pockets. Banks prepare by boosting reserve levels to cover potential loan losses. In the 12 months ending March 31, 2024, total loans at U.S. banks increased by 1.7% while loan loss reserves grew 8.2% (almost 5 times more).

That’s a sure sign that something is brewing. Now couple that with the previous 12 months when total loans grew by 7.5% and loan loss reserves grew 15.3%. That becomes more than a sign. The combination is a continued effort to replenish reserves that had been allowed to drop by more than 18% during the 12 months ending March 31, 2022.

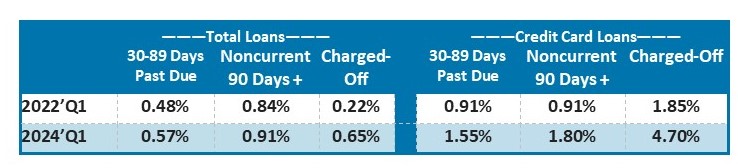

Remember two weeks ago? We told you commercial loans are not as bad as they appear (JRN 41:27). What we didn’t say (at that time) was that consumer loans are as bad as they seem, especially credit card loans.

In the past two years, total loans at U.S. banks increased 9.3%; loans to consumers grew slightly more at 10.8%. However, unsecured credit card loans grew more than 27%! The proportion of those loans that are falling behind (or worse) is just as telling:

These numbers were provided by the FDIC’s Quarterly Banking Profile (QBP) which looks at the banking industry in aggregate, but as we all know, not all banks are the same. That statement is true in many ways, but particularly when it comes to underwriting standards.

Next week we will examine banks that have been hit hard with credit card delinquencies. This week’s focus is intended to applaud those banks that increased loan loss reserves out of prudence, before it is actually needed. However, there are also some playing “catch-up”.

5-Star Barrington Bank & Trust, N.A., IL, is example of the former. Adding $3.9 million to its loan loss reserves in 2023 and provisioning another $2.3 million in the first quarter of 2024, Barrington B&T is diligently staying ahead of the need. Its leverage capital ratio (CR) of 10.64% is not much higher than its Bauer’s Adjusted CR of 10.56% because the vast majority of its delinquent loans carry government guarantees.

Additionally, Barrington B&T’s delinquent loans have actually been dropping, both from last quarter and from last year. As a precaution, Barrington B&T has increased its provisions anyway.

Barrington B&T is one of 52 banks listed on page 5 that are making an effort to beef up loan loss reserves. In each case, the allowance for potential loan losses increased more than 25% over a year ago. At March 31, 2024, each bank listed on page 5 also reported:

- delinquent loans (including loans in nonaccrual status) representing more than 1.5% of total loans (the national average is less than 1%); and

- loan loss reserves representing less than 70% of those delinquent loans (the national average is almost 200%).

Boosting reserves was a very smart move.

In some cases, like Barrington B&T, problem loans are not a real problem. These reserves will ensure they don’t become a problem down the line. Barrington B&T is an SBA lender and 43% of its loan portfolio is in Commercial and Industrial loans (C&I). The next biggest chunk is taken by 1-4 family residential real estate. Less than 15% of its portfolio is comprised of consumer loans. In this instance, none are credit card loans.

Now let’s examine a couple that are not so “well prepared”, like 2-Star Community B&T - W. GA. The difference between Community B&T’s Leverage CR (9.85%) and Bauer’s Adjusted CR (3.33%) tells a much different story here. In fact, loans past due 90 days or more or in nonaccrual status exceed 100% of Community B&Ts net worth—and that’s after a couple of sizable capital infusions.

Community B&T scraped through 2021 intact, with the help of one capital injection. Another this year is helping it stay afloat, but this bank just keeps taking on water. Delinquent loans grew by more than 400% in the 12 month period ending 3/31/24!

It could be worse (believe it or not): Zero-Star First & Peoples B&TC, Russell, KY, has a negative Bauer’s Adjusted CR (-1.82%). We reported on First & Peoples back in January (JRN 41:04) as a bank with precarious loan quality to keep an eye on. At that time we were looking at third quarter 2023 data.

Six months later things have only gotten worse for the beleaguered bank. A December enforcement action gave the bank six months to resolve some fairly major deficiencies, but a preliminary look at June 30, 2024 financial data does not reveal much, if any, progress. Apparently, First & Peoples got stung pretty badly by a third party loan program.

Be careful with whom you partner. That’s the moral to that story.