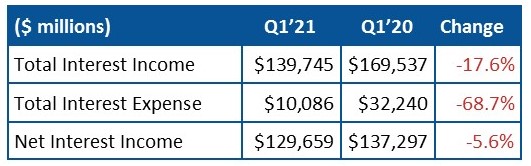

The average net interest margin at our nation’s banks contracted to its lowest level on record (2.56%) at March 31, 2021. In one year, the industry saw a decline of $29.8 billion in interest income, a decrease of 17.6%. If we told you that interest expense declined $22 billion in the same time-frame, it wouldn’t seem so bad. But it is:

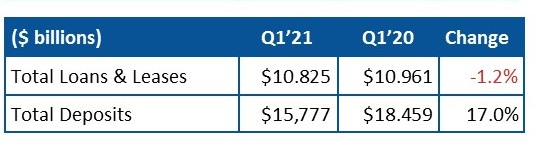

Much of the problem comes down to volume. Deposits have grown at a record pace during the pandemic. In the first quarter of 2021 alone, total deposits grew 3.6%. This includes: deposits in excess of $250,000 (up 4.7%) and noninterest bearing deposits (up 8.1%). And that’s just one quarter. Total twelve month deposit growth was a stunning 17%.

In addition to volume, during that 12 month period the cost of funds (the interest the bank pays for CDs, etc.) decreased 54 basis points to 0.20%, while the average yield on earning assets (what the bank gets paid in interest on loans, etc.) was down 1.1% to just 2.76%. Both of these are also record lows. Yet, over 64% of the industry reported higher net interest income than a year ago.

In addition to volume, during that 12 month period the cost of funds (the interest the bank pays for CDs, etc.) decreased 54 basis points to 0.20%, while the average yield on earning assets (what the bank gets paid in interest on loans, etc.) was down 1.1% to just 2.76%. Both of these are also record lows. Yet, over 64% of the industry reported higher net interest income than a year ago.

In theory, the greater the interest margin the more profitable the bank. In reality, when interest margins are squeezed, banks look for other sources of income. This can come in the form of fees, loan sales and/or securities and trading income. This year’s been different. Reversals of provisions made last year for anticipated credit losses (possibly prematurely) helped boost income.

The community banks listed on page 7 are still making their money on interest as each has a net interest margin well above the national average. We included the loan to deposit ratio on page 7 as well. While business models vary, a loan to deposit ratio (LTD) of 80% to 90% is generally considered optimal. At this level, the bank is lending sufficiently for its size, but not so much that its ability to meet other obligations could be compromised.

We also chose to only list community banks on page 7. This eliminates big banks, credit card banks, ILCs, and other specialty banks that we already know have different business models than your typical community bank.

Earning assets at each bank listed are doing exactly what they are supposed to do: earning. And quite well. To put them into perspective, compare any bank listed on page 7 to its peer group (by assets) below and to the 2.56% for the industry as a whole.

At the top of the list you will find 3½-Star Crescent Bank & Trust, New Orleans, LA, an $886 million bank with a 107% LTD, much higher than the “optimal” 80-90% and much higher than the 74.1% LTD of its peer group. Over 90% of Crescent’s loans are to consumers as it goes above and beyond to get people into vehicles who may otherwise be declined, not just in New Orleans but across the country. It’s a bit risky working with subprime borrowers, but the return can be much higher, as you see. On the downside, its past due loans (90 days or more + nonaccrual) are three times that of its peers. The next bank listed, 3-Star Kendall Bank, Overland Park, KS, is much smaller, with just $89 million in assets. Where Crescent Bank leans heavily toward consumer loans, Kendall Bank leans heavily (84%) in the opposite direction. Its loan portfolio is comprised of 40% Commercial & Industrial (C&I), 28% Commercial Real Estate (CRE) and 16% Construction and Land Development.

Kendall Bank was actually named the top lender for SBA loans by volume in Kansas. In the first quarter alone, it made 11 SBA loans totaling more than $10 million. As we all know, it isn’t just making the loans that matters, it is maintaining them in good standing. We are pleased to report that Kendall Bank currently exceeds its peers in every measure of loan performance.

So, why the 3-Star Rating? Kendall Bank has experienced some growing pains (it more than doubled in size between March 31 2020 and March 31, 2021). That, combined some other hiccups, has caused the bank to post several quarterly losses. Bauer is cautiously optimistic that this is a temporary condition.