All bank data and star-ratings are now based on year-end 2022 financial data, both in JRN and on bauerfinancial.com. One of the things we were excited to report last quarter was that Net Interest Margin (NIM) had widened to 3.14%. At year-end it has opened up even further, to 3.37%. The 82 basis point year-over-year NIM growth is the largest ever registered in the history of the Quarterly Banking Profile.

Bankers can thank the Federal Reserve’s persistent campaign of credit tightening for the increase. The Fed Funds rate has been boosted 4½% since the beginning of calendar 2022. But, at what cost?

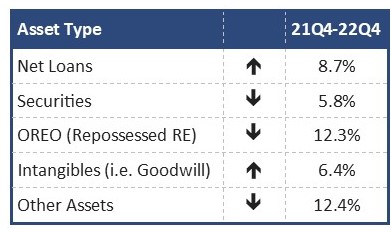

In spite of an increase in total loans and leases, fourth quarter bank assets were lower than both third quarter ’22 and fourth quarter ’21.

What’s worse, while total loans are growing, so are early stage past dues. Loans past due 30-89 days increased 18.9% from a year ago. Longer term delinquencies, 90 days or more in arrears, decreased by 10%, but net charge-offs increased by almost 90% (89.9% to be exact).

Provisioning went back from negative to positive as bankers brace for another possible recession. About two-thirds of the industry boosted loan loss reserve levels ...just in case.

All in all, and with a few exceptions, the banking industry took 2022, with all of its challenges, in stride. The industry ended the year with net income of $263 billion, which was down 5.8% or $16.1 billion from 2021, but that was primarily a result of the higher reserves.

However, we are all feeling the effects of inflation, including banks. Costs increased for bank premises and fixed assets as well as employee compensation. So, even with the closing of roughly 3% of bank branches during calendar 2022, overhead expense was up 5.5%.

For the third consecutive quarter, total bank deposits have fallen, but unevenly. Account holders are moving any money they had parked in uninsured deposits and either a) moving into insured accounts, or b) taking it out of the banking system altogether.

Since the close of 2021, total bank deposits have dropped 2.5%. Increased loans and decreased deposits brought the ratio of net loans to deposits up from 56.2% a year ago to 62.6% now. That’s one reason that FHLB advances are on the rise.

It has now been 28 months since the last bank failure, but, we lost 36 banks to mergers and acquisitions and seven ceased operations altogether during Q4’22. Three new banks opened for business during the fourth quarter as well, bringing the number of 2022 de novos up to 15. In all, we lost a net of 133 banks during calendar 2022 (2.7%). The three new welcome additions include:

3½-Star Bank Irvine, Irvine, CA

After receiving FDIC approval on July 28, 2022, that required initial capital of $25 million and a leverage capital ratio of 8% (or higher) Bank Irvine opened for business on October 18, 2022. Its intent is to provide banking solutions to the predominantly minority community of Orange County as well as the rest Orange and LA counties. By the end of 2022, Bank Irvine had $28.25 million in capital and assets of $39.2 million.

3½-Star Evermore Bank, Fort Lauderdale, FL

Evermore Bank received its FDIC approval on July 20, 2022. Its required initial capital to open was $25 million with a leverage capital ratio of not less than 8%. Evermore opened its doors on December 15, 2022 and at December 31st it reported assets of $37.038 million and capital of $27.776 million. It has already added a second location.

3½-Star Walden Mutual Bank, Concord, NH

After receiving its approval on September 26, 2022, Walden Mutual Bank wasted no time opening its doors. With the required initial capital of $22 million and a leverage capital ratio of at least 8%, Walden Mutual was open for business on October 5, 2022. Walden Mutual prides itself on “sustainable banking” with a focus on supporting the New England and New York local food economies.

Now, some less welcome news: Bauer’s Troubled & Problematic Bank Report and the FDIC’s “Problem Bank List”. Only two banks are considered less than “Adequately Capitalized” by Prompt Corrective Action (PCA) Standards. One, Zero-Star Village Bank, Saint Libory, IL, went all the way from Well-Capitalized last quarter to Significantly-Undercapitalized this quarter. That’s a huge jump, but that is only looking at capital levels. The FDIC currently reports that 39 banks (including Village Bank) are “problematic”.

Bauer’s T&P Report (all banks rated 2-Stars or Below) is also down from (48) last quarter, but contains 46 banks that Bauer considers to be less than “Adequate”. Remember, Bauer looks at the overall financial health of the bank, not just capital. What’s more, Bauer’s list is available to the public; the FDIC’s is not.