The commercial loan sector is one that continues to make news for all of the wrong reasons.

A list of 51 banks is provided in this week's issue of Jumbo Rate News that are each showing signs of stress in commercial loan portfolios, whether it be Commercial & Industrial, Commercial Real Estate, or a combination of the two.

Bauer's LLAMAS Report Bundle provides 5 quarters of data, including loan composition and quality, side-by-side to easily track a bank or credit union's journey along with graphs and ratios comparing it to its peers.

It’s Not the Water, It’s the Economy

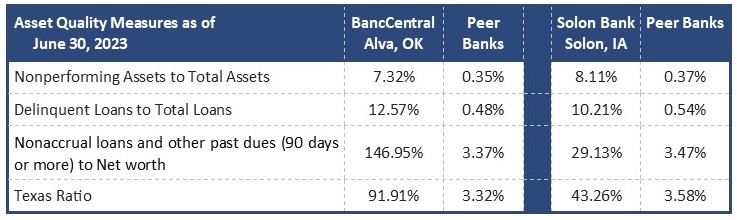

Last October (JRN 39:42) we reported that some banks had spooky numbers lurking in their business loan portfolios. With a delinquency rate of 11.2% on combined Commercial & Industrial (C&I) & Commercial Real Estate (CRE) loans, 2-Star BancCentral, NA, Alva, OK was one of those banks.

Its other loans were not faring much better as evidenced by a Texas Ratio of 110% and Bauer’s Adjusted CR of just 0.74%, but it is far from alone. In fact, BancCentral is one of 51 banks listed on page 5 showing signs of stress in commercial loan portfolios, whether it be C&I, CRE or a combination of the two.

In addition, each bank reports that over half of its loan portfolio is dedicated to commercial lending and at least 2% of those commercial loans are 90 days or more delinquent. The banks are each rated less than 5-Stars and also reported delinquent loans as a percent of total loans greater than 1.5% at June 30, 2023.

Recently, two major events have greatly impacted BancCentral.

- It has been operating under an Enforcement Action since November of 2021; and

- A new president and CEO, Taylor Horst, hopes to speed up the process of reigning these loans in.

To its credit, in the 12-months ending June 30, 2023, BancCentral:

- Improved from 1-Star to 2-Stars;

- Cut its asset size by about 1/3rd;

- And improved its capital position.

While it is still struggling with nonperformers, progress is visible.

Another bank striving to get off of this list is 3½-Star Solon State Bank, IA. But, with a hefty capital cushion, Solon State Bank has a leverage capital ratio of 21.24%, nearly double that of its peer group.

Yet, it continues to post higher and higher nonperformers. At June 30, 2023, Solon State Bank’s ratio of nonperforming assets to total asset exceeded 8%. That’s even higher than that of BancCentral, even though Solon State Bank’s other indicators are much stronger than those of BancCentral (see below).

You will also see several banks that have more recently developed issues in their commercial loan portfolios. (Some were listed in JRN 40:35, in a list of banks with overall worrisome loan quality.)

We noted that one of the banks from JRN 40:35, 3-Star Carter Bank, Martinsville, VA, reported much more than “modest deterioration” in its loan quality during the second quarter ’23. What we didn’t mention at the time, was that its neighbor, 3-Star Blue Ridge Bank, N.A., Martinsville, VA, was also struggling with loan quality. That’s two out of three banks headquartered in this small city.

The only other bank headquartered in Martinsville is a thrift: 4-Star Martinsville First Savings Bank, VA. As a thrift, 90% of Martinsville First SB’s loan portfolio is in single family residential loans. Conversely, both Carter Bank and Blue Ridge Bank, are most heavily invested in CRE.

Blue Ridge Bank has another folly, an affiliation with Fintechs, dozens of them. Last August (2022), the Office of the Comptroller of the Currency (OCC) slapped the $3 billion bank with an enforcement action relating, at least in part, to third party risk-management and Anti Money Laundering risk management related to those affiliations.

In May, Blue Ridge brought on a new CEO of its own, Billy Beale, to set things straight. Beale intends to cut ties with most, but not all, of the bank’s Fintech partners. It will no doubt be a slow process, but it has begun.

The Federal Reserve District 5 (Richmond, VA) reported in the latest Beige Book (released 10/18/23) several other regional issues that are not helping these Virginia banks:

- Development and construction of CRE was significantly reduced this period;

- Construction costs are historically high;

- Price growth remained stable across the region, yet labor costs continue to rise.

For financial institutions specifically:

- Maintaining deposits has become a struggle;

- Loan demand continues to slow, particularly real estate loans (both residential and commercial); and

- Institutions are monitoring credit quality and delinquency indicators as rates continue to rise.

Philadelphia, New York and Kansas City also reported slight declines in economic activity during the survey period. The other eight Districts reported stable or better economies during this Beige Book cycle.