All bank star-ratings and reports are now based on year-end 2020 financial data. (Credit Unions will be updated soon.) Three new banks opened their doors during the fourth quarter, bringing the total number of de novos for 2020 up to seven. While that’s only about half of the 13 de novo banks that opened in 2019, it is impressive given current circumstances.

Four banks failed in 2020 (two in the fourth quarter), four banks also failed in 2019. Merger and acquisition activity (M&A), not surprisingly, slowed during the pandemic. In 2019, 226 banks were absorbed by M&A. That dropped to just 168 in 2020 with only 31 completed during the fourth quarter.

At 56, the number of banks on the FDIC’s “Problem Bank List” remains the same as the previous quarter but is up from 51 at the end of 2019. Bauer’s Troubled and Problematic Bank Report currently includes 63 banks, which is down from 66 last quarter and 65 a year ago.

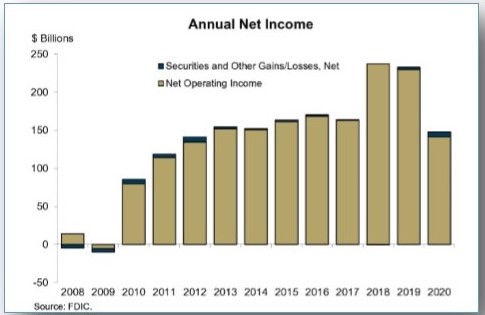

The net income at our nation’s banks for full-year 2020 dropped by over a third (36.5%) from 2019. At $147.9 billion, 2020 net income for the industry was its lowest since 2012 (see graph). The decline was largely attributed to allowance for loan losses due to the pandemic.

For the most part, those allowances were in the first half of 2020. Quarterly net income at 12/31/2020 was actually 9% higher than fourth quarter 2019. In fact, more than half of all U.S. banks reported year-over-year increases in net income. Many, if not most, did so while also increasing their loan loss allowances. The 50 with the highest year-over year increase in annual net income can be found on page 7.

One caveat to this list is that, in ordering by percent income growth, if they posted a loss in 2019, they were excluded. The first few listed were barely profitable in 2019, which is why the numbers seem so crazy. In any case, their boards are surely happy.

Another thing we should mention is that some of these banks were acquirers during 2020. If you look about half way down, 5-Star Border Bank, Fargo, ND reported large increases in net income, loan loss allowance and assets (not shown). That was due to the acquisition of Union State Bank of Fargo in December. Border Bank is an exception, though. The majority of the banks listed saw net income grow organically and generously.

You also may wonder why some banks are reducing loan loss provisions. 5-Star One American Bank, Sioux Falls, SD reduced its reserves by 27% charging off $1.8 million in delinquent loans in 2020. Its reserve to delinquent loan ratio is still 361%. 5-Star Waterman State Bank in IL also cut its reserves, by almost half in 2020. Waterman has no delinquent loans on its books.

Then there are banks like 2-Star Brighton Bank in TN. Brighton Bank, which even though it increased its loss allowance by a third, still has barely enough to cover half of its delinquent loans. While it has been working to reduce bad loans, Brighton Bank’s loan underwriting history has been what we will call “questionable”. But it is working on it.

A year ago, Brighton Bank’s nonperforming asset ratio was 3.9%; reserves were enough to cover just 39.5% of delinquent loans; Bauer’s adjusted capital ratio was just 3.12%; and its Texas Ratio was pushing 50%.

A pandemic and twelve months later and its delinquency to asset ratio is down to 2.2%; its reserves to delinquencies are 51%; Bauer’s adjusted capital ratio is 4.9%; and its Texas Ratio is under 30%. So, there is improvement.

You can find more information on Brighton Bank and all 63 banks rated 2-Stars or below by Bauer on our Troubled and Problematic Bank Report. A pdf version is just $99 Excel® spreadsheet with contact information is $225. Both are available for immediate download.