The banking sector is generally strengthening, with higher earnings, stable asset quality, and fewer problem banks, though some risks remain.

For example, asset quality remained stable overall, with a slight improvement in total past-due and nonaccrual loans, though some loan categories still show elevated delinquency levels.

Bank deposits continued to grow …including a notable increase in estimated uninsured deposits.

JRN by Bauer 43:21

New Bank Ratings Now Out, Based on March 31, 2026 Data

All bank star-ratings have now been updated based on March 31, 2026 financial data. As a result, some banks have changed star-rating categories. We suggest you visit bauerfinancial.com to check the ratings on banks you do business with. Credit union data and star ratings are expected to be available by the middle of June, but we’ll let you know for sure when they are actually available.

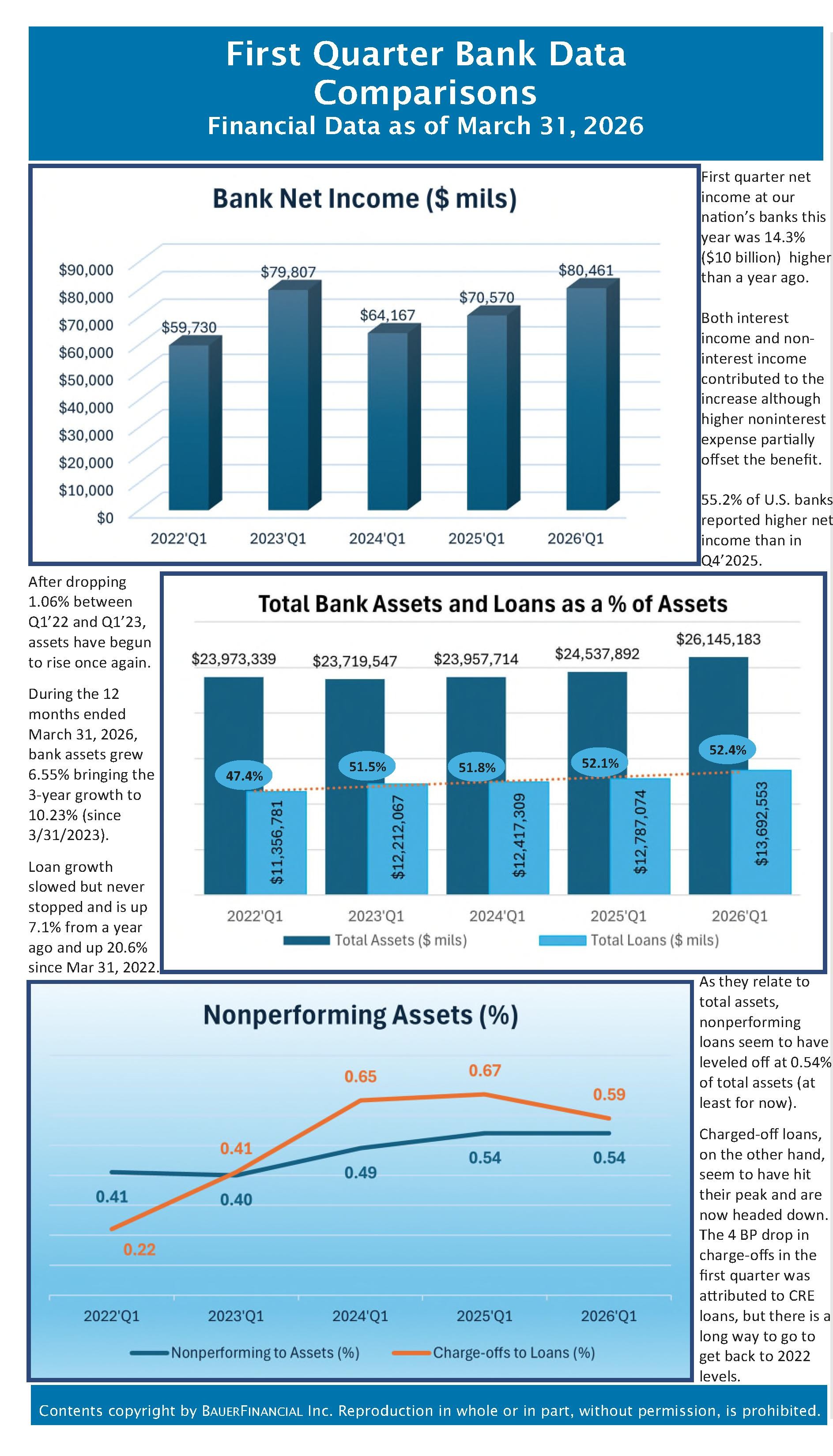

As for banks, the first quarter was highlighted by a rise in net income. Quarterly net income was $10.1 billion (14.3%) higher than a year ago (see page 5 graphs) and 3.9% higher than fourth quarter 2025. Over 55% of banks reported higher net income at March 31st than in the previous quarter and less than 5% (4.8%) of the industry reported a first quarter loss.

The yield on earning assets (loans, etc.) was down 21 basis points (BPs), in the first quarter. When coupled with a decrease of just 13 BPs on the cost of funds (e.g. interest paid on deposit accounts), the result was a decrease in net interest margin (NIM) from 3.39% at year-end to 3.31% at March 31.

Noninterest income saw first quarter gains of $5 billion (5.8%) so, despite a $1.6 billion decline in interest income, net operating revenue increased in the first quarter (up $3.4 billion or 1.2%).

Loan loss provisioning expenses were up (2.3%) from year-end, but noncurrent loans increased 3.3%. As a result, the reserve coverage ratio (allowances for credit losses to noncurrent loans) dropped from 171.2% at year-end 2025 to 166.8% at March 31st.

That brings us to asset quality which is still holding up nicely at most banks. Overall, loans past due (30 days or more) and nonaccrual (PDNA) were down slightly (3 BPs) to 1.53% from previous quarter, with credit cards and other loans to individuals showing the most improvement. However, we still see elevated levels in many categories.

| Loan Type | PDNA Q1’2026 | PDNA Q4’2025 | Change | BPs |

| Credit Cards | 3.08% | 3.15% | Down | 7 |

| Other Loans to Individuals | 2.14% | 2.42% | Down | 28 |

| Home Equity Lines | 2.10% | 2.13% | Down | 3 |

| Other 1-4 Family Residential | 2.08% | 2.02% | Up | 6 |

| Nonfarm nonresidential CRE | 1.66% | 1.63% | Up | 3 |

| Multifamily CRE | 1.47% | 1.42% | Up | 5 |

| Construction & Development | 1.40% | 1.34% | Up | 6 |

| Commercial & Industrial (C&I) | 1.37% | 1.39% | Down | 2 |

| All Loans and Leases | 1.53% | 1.56% | Down | 3 |

Domestic deposits at U.S. banks grew for the 7th consecutive quarter. This time by 1.2% or about $390 billion. Gains were seen in both interest-bearing and noninterest-bearing deposits accounts. However, it was the increase in estimated uninsured deposits that really caught our eyes.

Based on the roughly one-quarter of banks that report uninsured deposits, the amount was about 3% higher at March 31st than at year-end and 9.7% higher than a year ago.

And finally, the number of banks on the FDIC’s Problem List (those with CAMELs ratings of 5 or 4) decreased by a net of six to just 54 banks at March 31st. (There were three additions and nine removals.)

Some of these highlights are graphed (page 5), but we would like to revisit some of the banks from last week’s article. If you recall, last week we listed 52 banks that each had:

- A Bauer Star-Rating <= 3½-Stars;

- Assets consisting of at least 30% loans;

- A loan portfolio with at least 25% residential real estate loans; and

- At least 1.5% of residential real estate loans were nonperforming (based on year-end ’25 data).

We already had a sneak peak into 3½-Star Priority Bank, Fayetteville, AR (33818) last week, so we’re not surprised to see it still meets these criteria. Priority Bank is a $150.6 million asset bank with $113.6 million in loans, about 62% of which are residential real estate loans. While growth in Priority Bank’s residential loan portfolio slowed some from the previous quarter, the portion reported as delinquent rose slightly. It now sits at 4.29%, up from 4.23% last quarter.

When we look at Priority Bank’s overall loan portfolio, however, we do see improvement. Its leverage capital ratio (CR) went from 10.04% to 10.81%; Bauer’s adjusted CR went from 7.53% to 8.81% and its Texas Ratio dropped from 24.54% to 18.75%. That marks quite an improvement in the overall loan portfolio.

Another, Apex Bank, Camden, TN (9176) improved to a 4-Star Rating with March 31st data. The $1.4 billion asset bank slowed its residential real estate lending growth rate in the first quarter. The delinquent share of those home loans also showed improvement—from 1.94% at year-end to 1.87% as of March 31. Apex Bank maintains a solid capital cushion, with a leverage CR of 14.45%, a Bauer’s adjusted CR of 12.70%, and a Texas Ratio of 13.13%.

Although there are caveats, the industry is showing improvement. For individual bank ratings, please visit bauerfinancial.com.