People sometimes can’t find a bank’s rating on Bauer’s website due to naming, location, or search errors, but occasionally the bank truly isn’t listed.

This is because certain foreign bank branches—allowed under laws like the International Banking Act of 1978 and later “grandfathered” by the FDIC Improvement Act of 1991—have FDIC insurance but no U.S. charter.

Since these branches don’t file full financial reports, Bauer lacks sufficient data to rate them and only evaluates banks with both FDIC insurance and a U.S. charter.

JRN by Bauer 43:22

The Case of the Missing Bank Rating

Every so often, we get a phone call at Bauer from someone unable to find a particular bank rating on our website. There are several reasons this can happen (the caller may be looking for a specific location while we list banks by their headquarter location; the bank may be commonly known by initials or a shorter version of its legal name (which is what we list); and sometimes it’s as simple as a typing error).

Occasionally, however, we get a call from someone who has the FDIC certificate number in hand and is still unable to find the bank’s rating on bauerfinancial.com. How can that be if Bauer rates all federally-insured banks that have a U.S. charter? Naturally, they call us.

Bauer has been around for well over 40 years. We know how this anomaly came to be and what caused it. Most people have no idea, though, so today we will explain it.

Bear with us, please. It starts with a history lesson. We have to go back almost half a century to The International Banking Act (IBA) of 1978. The IBA provided a way for foreign banks to establish federal branches (or agencies) in the U.S. It also allowed them to take deposits, regardless of whether they carried FDIC-insurance coverage.

While there were limitations, foreign banks interested in deposit-taking in the U.S., upon approval by the OCC, Federal Reserve and FDIC, could now establish a “Federal” branch in the U.S. with FDIC deposit insurance. Prior to this, some states allowed foreign banks to obtain a state charter, but intentionally or not, the IBA opened a path to FDIC deposit insurance for these existing state branches as well.

Fast-forward to the 1980s and the Savings and Loan Crisis. Over the course of the decade, over 1,200 banking institutions failed, others needed assistance to stay afloat. The deposit insurance fund was rendered undercapitalized. Enter the FDIC Improvement Act of 1991 (FDICIA).

Primarily known for Prompt Corrective Action (PCA) and least cost resolution requirements, the FDICIA also prohibited de novo branches of foreign banks from obtaining FDIC insurance coverage. Existing branches that already had FDIC insurance coverage, however, were “grandfathered” in, allowing them to keep that coverage. Between 1978 and 1991, the door was wide open to foreign banks.

At the end of 2018, 130 foreign banking organizations (FBOs) operated in the U.S., some via U.S. chartered banks, others through a non-chartered branch or agency. Most of these branches/agencies were quite small. Importantly, however, while the domestic branch was small, the FBO itself was almost always systemically important in its home country and many were also Globally Systemically Important Banks (G-SIBs) as well.

The passage of Dodd-Frank in 2010 laid out new guidelines for foreign banks, imposing new regulations and capital standards which ultimately increased regulatory costs. These higher costs led to a decrease in the number of foreign bank branches/agencies we have in this country. Some banks cut back their U.S. operations (or left the U.S. altogether), others consolidated their existing “foreign” branches/agencies into U.S. affiliates. And seven, mostly European, failed due to a concurrent European financial crisis.

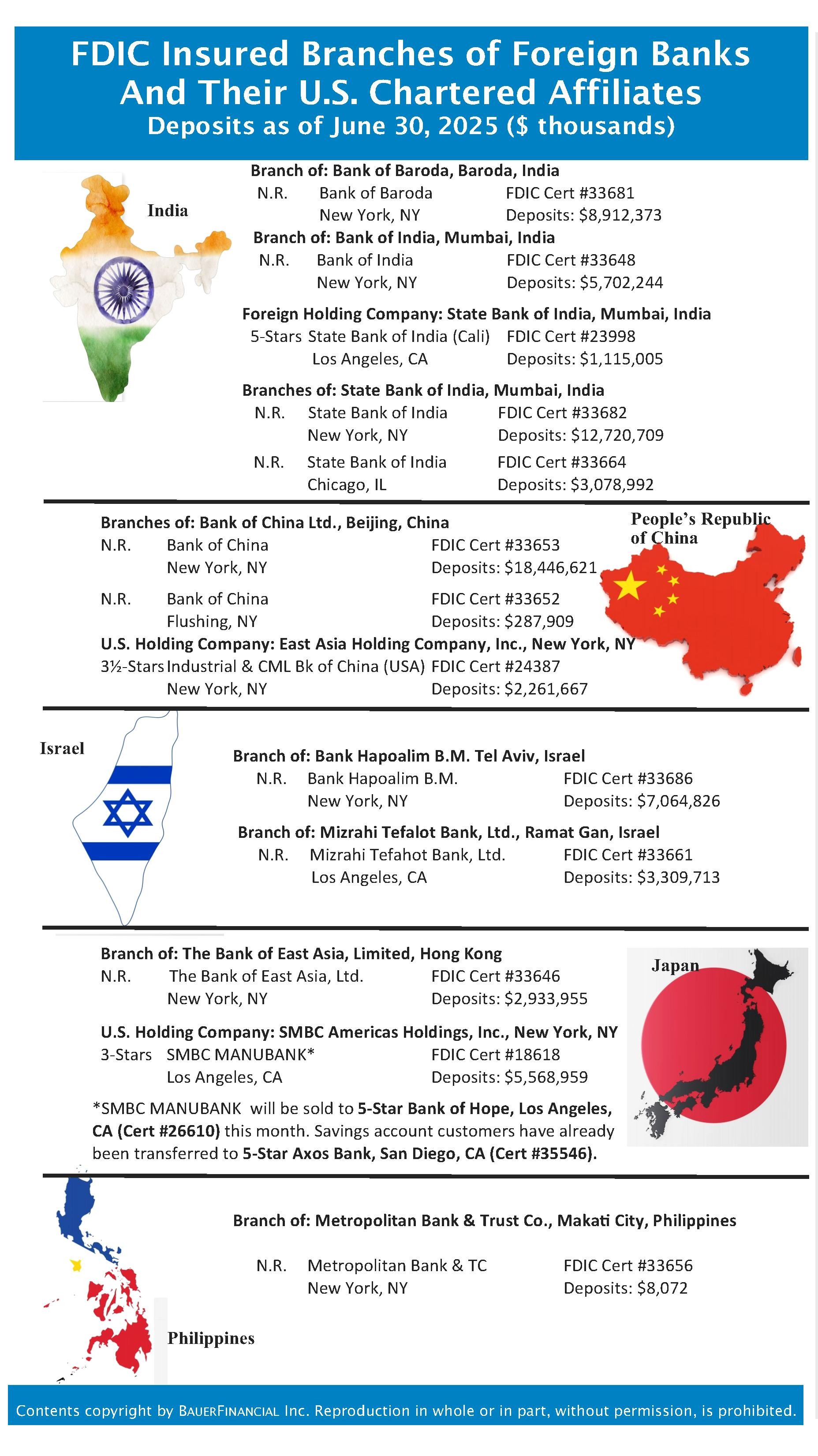

Since the passage of Dodd-Frank, we’ve lost U.S. affiliates from Europe, Asia, Mexico and South America. We also gained some, mostly from Asia and South America. Of the “grandfathered” insured branches of foreign banks, ten are still in operation today (depicted below).

Whether from Dodd-Frank or Basel, or a combination of the two, U.S. bank regulators now look closely at the home country of a bank to determine if it poses risk to the stability of the U.S. The Federal Reserve can close a branch or agency of an FBO if it determines the home country is unable to mitigate systemic risk if the parent bank were to fail. In other words, the home country regulators have to be up to par with ours.

In addition, banks with $50 billion, or more, in U.S. assets were newly required to form a holding company for all of their U.S. holdings. This holding company must meet all of the same requirements as any other U.S. holding company (capital ratios, liquidity, living wills, etc.). This added another layer of protection for the U.S. as well as the global economy.

The foreign banks that have U.S. charters (state or federal) file quarterly call reports like every other U.S. bank. We have the information to evaluate and rate them. The ten “grandfathered” insured branches of foreign banks do NOT file quarterly call reports and are therefore not rated by Bauer.

While we do have limited data from the Federal Reserve, it is not enough. Therefore, Bauer will never rate a bank that doesn’t have both FDIC insurance and a U.S. charter. That solves the case of the missing bank rating.