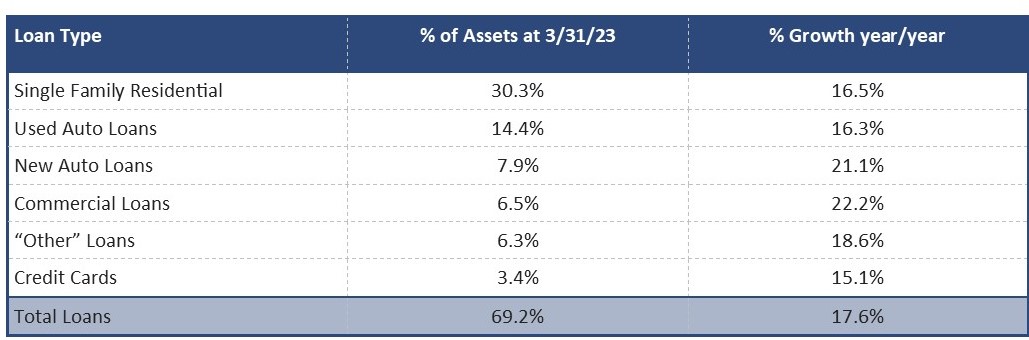

First quarter 2023 credit union data is all about loans. After jumping 17.6% from a year ago, total loans outstanding at federally insured credit unions now top $1.5 trillion. At $17,310, the average loan balance was up almost 6% from a year ago. Total assets, however, grew by just 4.4% over the 12 month period. Loan balances rose in all major categories from a year ago.

As those loans climb, so does the percent that is not performing. At March 31, 2022 delinquent loans at credit unions totaled $5.5 billion for a delinquency rate of 0.42% (which is quite good). A year later and those delinquencies have grown to $8 billion (46%). That sounds like a lot, and it is, but with a delinquency rate now at 0.53%, we are not worried about overall loan quality.

Every rule has its exception and credit card delinquencies are the exception to this one. Delinquent credit card loans remain stubbornly at 1.48%, the same place they were last quarter but 47 basis points above where they were a year ago.

The net charge-off rate has also climbed...precipitously. It more than doubled (121% increase) in the past 12 months to 0.52%. To keep this from becoming a problem, credit unions put aside $8.8 billion in loan loss provisions during the quarter. That’s over 200% more than the provision expense from a year ago.

Aside from the loan loss provisions, noninterest expense remained inline with last year. Interest expense, as you can imagine, has had nowhere to go but up. A year ago, the credit union industry interest expense was 0.35% of average assets. Today, it is 1.06%. And it will continue to climb as long as the federal reserve keeps raising interest rates (which it paused at this week’s meeting).

For the same reason, interest income has also climbed. Last March, interest income accounted for just 2.92% of average assets but today it accounts for 4.07%. Because of that, the aggregate net interest margin increased by $12.2 billion (22.6%) over the year.

The 52 credit unions listed on page 5 of this week’s Jumbo Rate News each reported more than 50% loan growth during the 12 months ending March 31, 2023. To make the list more meaningful, we limited it to credit unions where loans account for more than 50% of total assets. In addition to loan growth, you will find the delinquency to asset ratio for each institution as well as loan loss allowance as a percent of delinquencies.

We are going to take a closer look at a couple of the credit unions on the list. But, before we do, let us say the industry as a whole is in quite good shape. Based on first quarter 2023 numbers, 85% of federally insured CUs (FICUs) were profitable (compared to 77% a year ago) and 83% earned a recommended rating of either 5-Stars or 4-Stars from Bauer (virtually unchanged from a year ago).

Median loan growth at FICUs during the 12 months ended March 31, 2023 was 13.3, but that varied greatly by state. Rhode Island was one of the states with a lower median (between 10 and 12%), yet one Rhode Island credit union made our page 5 list.

Established in 1946, 5-Star Cranston Municipal Employees Credit Union, Cranston, RI has total assets of $75.3 million. After witnessing a 12 month surge of over 117% in its loan portfolio (almost half of which are first mortgage real estate loans), $41.6 million of its assets are now loans. (A year ago, loans represented less than 27% of total assets.)

So far, the quality of those loans is excellent, with just 0.03% delinquent (compared to 0.59% for its national peer group and 0.25% or less for Rhode Island). Cranston Municipal’s reserves are sufficient to cover 955% of its current delinquencies and 0.25% of its total loan portfolio.

Not doing quite as well is 2-Star 1st Choice Credit Union, Atlanta, GA, which is working hard to turn its loan situation around. At March 31, 2022, 45% of 1st Choice’s loans were unsecured and another 45% were auto loans. Today, 18.7% are unsecured and 62% are auto loans. The unsecured portion is still high compared to its peer group’s 11%.

Unsecured loans are also the most difficult to collect on. In the 12 months ending March 31, 2023: total loans have grown 98%; but delinquent loans have grown 620%. As a result, 1st Choice CU’s nonperforming asset ratio has ballooned to 5.8% while that of its peer group is just 0.4%. The median delinquency rate for the state of Georgia is right in line with the peers at 0.35% to 0.45%.

The state with the highest percent of loan growth during the 12 months was Nevada with median growth of 20.3%. Yet, no individual Nevada credit unions can be found on page 5.

The state that reported the highest median delinquency rate was New Jersey at 0.88% and the lowest was Utah at 0.13%. The median delinquency rate for the nation was 0.38%.