A timely confirmation is expected for Kevin Warsh to be the next Federal Reserve Chair, with Jay Powell remaining on the Fed’s board until his term ends in January 2028 (awkward).

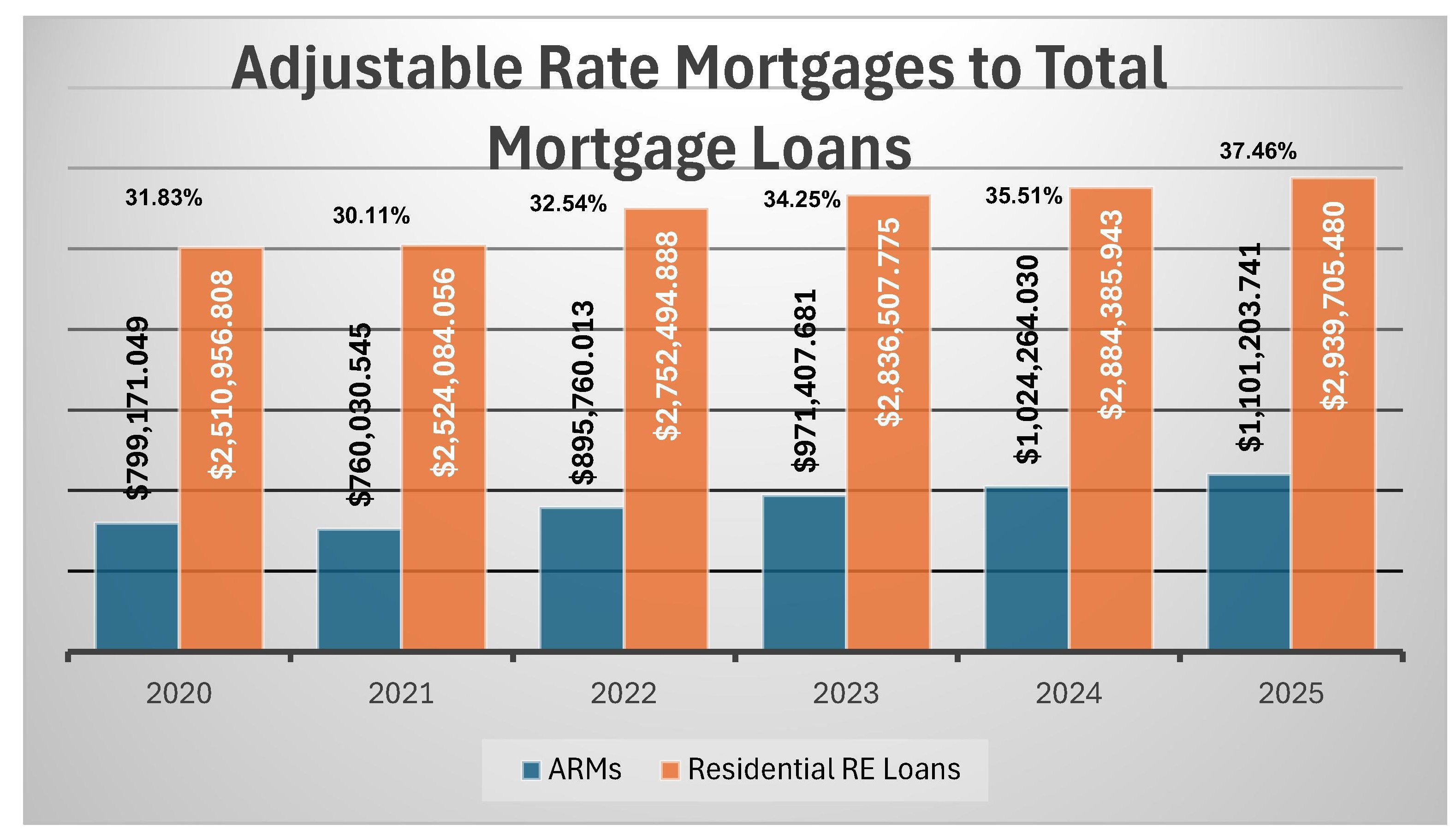

While we don't know exactly what will happen with rates in the near-term, we do know adjustable-rate mortgages (ARMs), which move with the Fed Funds Rate, can pose a risk. If rates rise, ARM payments will increase quickly, potentially pushing already inflation-stressed consumers into delinquency.

JRN by Bauer 43:17

Rate Risk Worries Returning to the Picture

All indications currently point toward a timely confirmation of Kevin Warsh as the new Chairman of the Federal Reserve. Jay Powell has decided to remain on the board until his term ends on Jan. 31, 2028.

We believe that once he gets into office, Mr. Warsh may have a harder time than he bargained for trying to a) tame inflation, b) support maximum employment, and c) forge a consensus among voting members of the Fed’s Open Market Committee (FOMC). (We believed that even prior to Powell’s decision.)

Although the Fed Funds rate did not change this week, it will eventually. The question is, in which direction? We indicated last week that, with Warsh at the helm, rates would come down sooner rather than later (JRN 43:16), but that was just comparing to Powell’s timeline.

The reality of stepping into one of, if not the most, influential banking positions in the world, must (should) come with an ounce of humbling and a pound of patience. Incoming data needs to be carefully evaluated before any moves are made.

As we also mentioned last week, we are looking at adjustable-rate mortgages (ARMs) in this issue. Rates on ARMs swing with the prime rate, which hinges on the Fed Funds Rate. If the Fed Funds Rate goes up, rates on ARMs will quickly follow. If the Fed Funds Rate goes down, rates on ARMs will also follow.

Each bank listed on page 5 of this issue has at least 20% of its loan portfolio invested in residential loans AND at least 18% of total loans are ARMs. As you will see, some are much higher than 18%.

As consumers are already feeling squeezed with inflation, an increase in the monthly mortgage payment could send some into arrears. Note: this list does not include home equity lines of credit (HELOCs), which have the potential to spur their own dire consequences.

2-Star Fieldpoint Private Bank & Trust, Greenwich, CT (58741), for example, has total assets of $944 million. Of that, $658 million is in loans, about 44% of which is invested in single family residential, in some format.

At year-end 2025, 1st lien single family mortgage loans totaled $230.749 million (approximately 31% of which are ARMs). Another $56.98 million was HELOCs.

Non-performing 1st liens were reported at $962,000 (0.42% of the total, including ARMs) while non-performing HELOCs of $1.583 million constitute 2.78%.

This demonstrates the importance of every type of loan and every item reported on the call report, but there are not enough weeks in the year to deep dive into each one.

Rest assured that Bauer’s star-rating takes all of this information (as well as historical data) into consideration. Fieldpoint’s 2-Star rating is and overall rating of its health and strength.

Another 2-Star rated bank, Eastern National Bank, Miami, FL (20026) decreased both its total assets and loans by 35% and 41% (respectively) during calendar 2025.

We last reported on Eastern NB last September (JRN 42:37) when we wrote it, “has been operating under a consent order since October 2018. Not the same order, mind you. The order has been replaced twice because the bank failed to meet the original terms of the first agreements.”

That article, was appropriately titled “Banks Want to Grow, Why are These Banks Shrinking?” In 2025, Eastern NB posted another $3.129 million loss and lost another $3.089 million in capital (hand in hand).

While Eastern NB’s problems have little, if anything, to do with ARMs, almost 74% of its residential real estate loans are subject to rate changes. That could become another issue for this shrinking violet.

If you need yet another reason to look at the entire picture of a bank, look no further than the $25 billion asset 3½-Star Ameriprise Bank, FSB, Minneapolis, MN (58303). In 2025, its loan portfolio grew 46.5%. Of nearly $2 billion in total loans, about $800 million (41%) is in residential real estate, and 44% of that amount ($351.313 million) is in ARMs.

Based on year-end 2025 data, $2.326 million of these mortgages are nonperforming. That’s not bad, only about 0.3%. If you add the short-term past dues (30-89 days in arrears) the number triples to $9.044 million (about 1.1%).

That’s still not horrible, except its credit card loans are also seeing increases in short-term past dues. In a worst-case scenario, Ameriprise Bank’s delinquent loans could conceivably jump from $3.324 million to $11.235 million over the quarter. While that is highly unlikely, it is certainly something we will have an eye out for. (Its March 31, 2026 Call Report was not yet available as of this writing.) Loan loss reserves of $11.284 million are enough to cover almost the entire amount in the unlikely event it is needed.

Here’s the catch. Ameriprise started off as a financial advisor. It just became a bank in 2006. As a result, net loans only amount to 6.5% of total assets, far below its peer group’s 73.8%. The mix is changing, but it’s a process and slow is the prudent way to go.