Alan Greenspan, longtime Federal Reserve chairman, remains a controversial figure—praised for guiding economic prosperity but criticized for missing risks that led to the dot-com and housing bubbles. To assess his impact, it’s important to understand the turbulent economic backdrop before his tenure.

By the time Greenspan took office in 1987, he faced immediate challenges like the stock market crash but stabilized markets with decisive action.

Greenspan skillfully managed the Fed’s dual mandate of low inflation and employment, while also becoming known for his vague and carefully worded communication style, often called “Greenspeak.”

JRN by Bauer 43:25

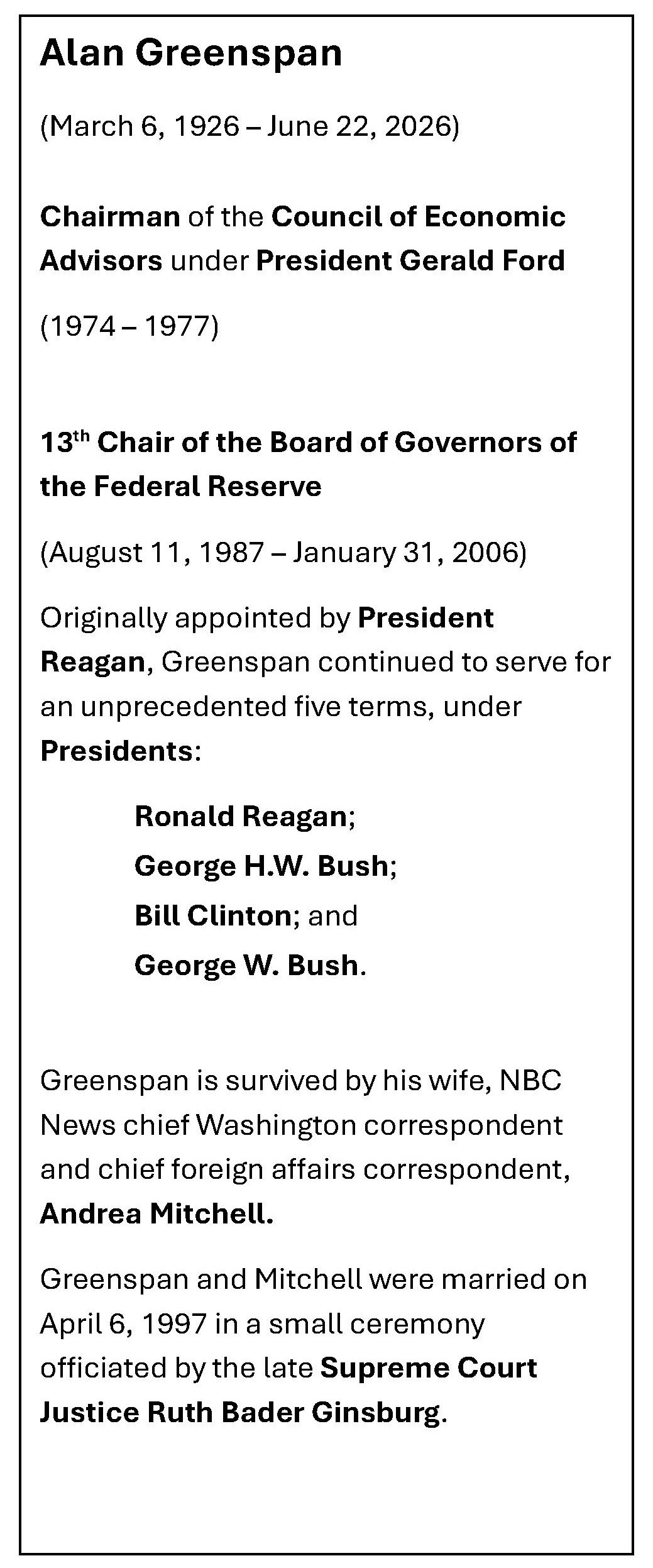

Rest in Peace, Maestro

Some people loved him. He orchestrated the markets and created a generation of prosperity.

Others blamed him for not recognizing the risks that were building and eventually led to the dot-com (2001) and housing (2008) bubbles.

Regardless of where you stand, there is no doubt Alan Greenspan left his mark. For decades under four presidents (both parties), he worked to shape our economy as if conducting an orchestra.

To truly evaluate the efficacy of Greenspan’s 19-year tenure, however, we need to take a look backwards and examine what was going on before he became Chaiman of the Federal Reserve.

Financial markets experienced extreme turbulence in the 1970s and 1980s, particularly in banking. Those of us who remember the 1970s can still recall the double-digit inflation and the OPEC oil crisis causing long lines at the gas pumps.

On the political front, the Watergate scandal culminated in Richard Nixon’s resignation (August 9, 1974), but not before he put an end to our involvement in the Vietnam War.

Other events from the 1970s could be ripped from the papers today (if we still had papers). Russia invaded Ukraine and the Camp David Accord gave us new hope for peace in the Middle East. Then in 1979, Iran took 52 American hostages and held them captive for 444 days. Hope of peace in the Middle East was lost and consumer sentiment in the U.S. took a nosedive, too.

With all this turmoil, most Americans did not realize how much pressure was building on the nation’s banks. After the Great Depression (1929–1939) and the resulting Banking Act, also known as the Glass-Steagall Act (1935), established the Federal Deposit Insurance Corporation (FDIC), restrictions on the banking industry continued to grow. With little competition for deposits, banks paid very little on savings while earning much higher interest on loans. Margins were wide, and despite increasingly heavy regulation, bankers were generally content.

Enter Arthur F. Burns. Nominated to chair the Federal Reserve by then President, Richard Nixon, Burns became chairman on February 1, 1970, and remained chairman for most of that decade. In a cautionary tale of why the Federal reserve must maintain its independence, it is widely believed that Burns, an inflation hawk, allowed Nixon to influence him into keeping rates low to help him get re-elected. Nixon was re-elected in 1972, but the low-interest rate environment caused inflation to soar. In fact, the period from 1965-1982 would later be dubbed The Great Inflation.

In 1971, a new money market fund was introduced specifically for people with less than $100,000 to be able to invest. This new product dramatically altered the way Americans save. For the first time since deposit insurance was created, banks had direct competition as these instruments were only available through brokerage firms.

At that time, regulations restricted the interest rates that banks could pay to between 5-5.25%. These new funds were paying 8% or more. Consumers began shopping for yield and bank profits were reduced drastically. Both Arthur Burns and his successor, G. William Miller, witnessed the exodus of Federal Reserve member banks as banks tried anything they could to cut costs.

It was not until Fed Chairman Paul Volcker took the helm (August 1979) that he, along with then President Jimmy Carter, enacted the Depository Institutions Deregulation and Monetary Control Act of 1980, that banks were again able to compete for deposits. And compete they did.

This law also, for the first time, enabled savings and loans to offer commercial loans, trust services and NOW Accounts (checking accounts that pay interest). Money Market Deposit Accounts were added to the list in 1982.

Savings and Loans were inexperienced in these departments. They were in the business of taking in deposits and using them to finance homes. All they knew about these new freedoms was enough to get themselves into trouble, and that they did. Some innocently enough, made bad loans or invested in junk bonds pedaled by unscrupulous brokers. Others, not so innocently, blatantly and fraudulently used the deposits as their own private piggy banks. During the 1980s, over 1,000 savings and loans failed as an indirect result of deregulation.

When President Ronald Reagan took office (1981) he kept Volcker on for another term, but by 1987, Volcker was exhausted. He reportedly requested he NOT be renominated, although he did remain until Reagan could find a suitable replacement.

On August 11, 1987, Alan Greenspan was sworn in as Chairman of the Board of Governors of the Federal Reserve. (It took a minute, but we did get back to him.) Greenspan took office just two months before Black Monday (October 19, 1987), when the Dow Jones Industrial Average fell 22.6% in a single day. The resulting panic dissipated as the Fed assured markets it would provide much needed liquidity to weather the storm. It was a trial by fire and Greenspan emerged a hero.

Between 1991 until his last term expired in 2006, the annual inflation rate never reached 3.5% and was often below the Fed’s benchmark 2%. However, 2001brought with it the dot-com bubble. Greenspan and the Fed had to lower interest rates to keep the economy rolling. He started cutting the Fed Funds target before the ensuing recession began and sped up the cuts between December 2000 – December 2001.

Despite these deep rate cuts (from 6.5% to 1.75%), he could not keep us out of a recession. The terror attacks of 9/11/2001 exacerbated that outcome. The recession officially lasted 8 months (March 2001 – November 2001). Rates continued to come down until the Fed Funds target rested a 1% for about a year (July 2003 – June 2004).

While Greenspan could not prevent the dot-com bubble, the highest unemployment rate during his tenure was 7.8% (June 1992) and the highest inflation rate was 6.11% (1990). Under Volcker, unemployment reached 10.8% (October 1982) and inflation peaked at 13.3% (1980). Yet, to this day, Paul Volcker is regarded as the “Knight who tamed inflation”.

Granted, Volcker walked into a much bigger mess when he took the helm in 1979 than what he left for Greenspan in 1987. That does not take away from how Greenspan tackled the dual mandate of the Fed (maximum employment and low inflation) with consistent precision. We had a first-hand view of how Mr. Greenspan orchestrated the markets and it was always entertaining to watch.

Understanding him, however, was another story. Even his wife, Andrea Mitchell, joked that Alan had to ask her to marry him three times before she understood what he was asking. In media interviews, he had a way of telling you enough to satisfy your thirst for an answer without spilling any real information. Greenspeak, as it became affectionately known, was an art form that not many mastered… although, it looks as though our new Fed Chairman, Kevin Warsh, may have taken some lessons.