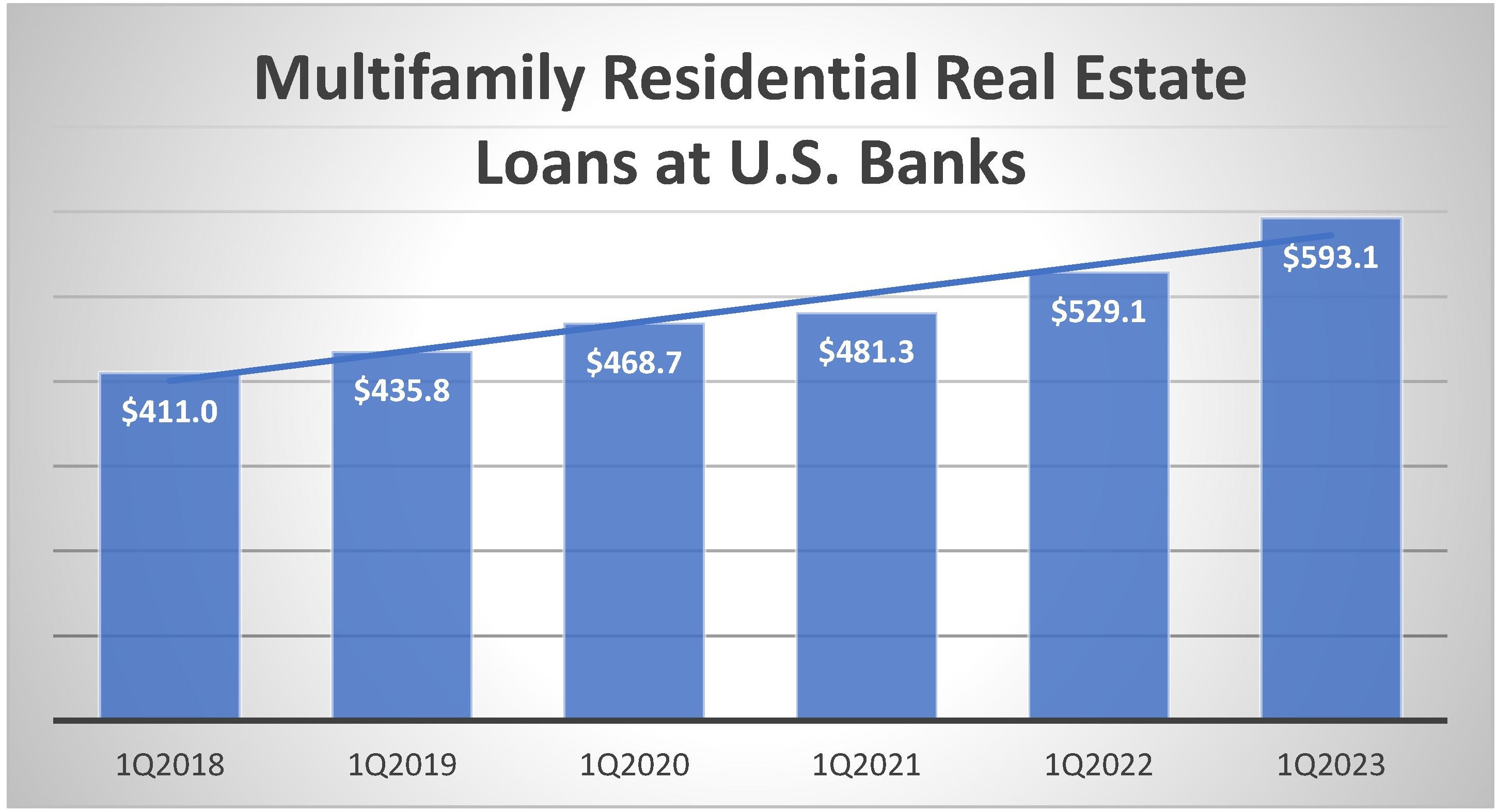

Fact: Multifamily Residential Real Estate Loans have grown over 44% in the past 5 years.

Top Lenders: JPMorgan Chase Bank, N.A., Columbus, OH is by far, the top lender of this type, however, 50 U.S. banks have at least one-third of their loan portfolio in multifamily residential real estate loans. They are listed on page 5 of this week's Jumbo Rate News.

Other Resources: Bauer's Due Diligence Performance Report

Should Multifamily Residential Real Estate Worry Us?

We have reported several times in the past few years on Commercial Real Estate (CRE) (most recently in JRN 40:23). We focus on if and when it is time to get worried about certain aspects of CRE. What we have not honed-in on specifically, is multifamily residential real estate loans. Today we are going to rectify that.

In the past five years (from first quarter 2018 to first quarter 2023), the dollar amount of multifamily residential real estate loans outstanding at U.S. banks increased nearly 45% (from $411 billion to over $593 billion). That seems like a lot considering the droves of residents who fled crowded buildings for single family homes during the pandemic.

Inflation explains some of the increase, but the amount of total loans grew at a much slower, 25.3% rate, during those five years. What made multifamily loan growth outpace total loan growth and will that play a part in the repayment of those loans?

According to The U.S. Census Bureau, the vacancy rate for residential rentals in 2018 ranged from a low of 6.6% to a high of 7.1%. By the second quarter of 2020, the vacancy rate had dropped to 5.7%. It has been moving in anything but a straight line since, but for the past year, the general trajectory is up. By the end of the first quarter 2023, the vacancy rate was up to 6.4%.

All other things being equal, a higher vacancy rate indicates there are fewer people competing for apartments. Less demand means landlords may have to reduce their rent to entice renters. The problem with that is that property values haven’t gone down, nor have taxes or insurance. In fact, all costs associated with owning a rental property have risen with inflation.

If the vacancy rate continues to climb, this could become a problem for the building owners. It depends on several other factors as well, though. When was the property purchased? How much equity does it have? What is the interest rate? What kind of cushion is set aside for slow rental seasons?

The answers to these questions will vary tremendously depending on the borrower and also on the lender. A prudent lender will do its best to make sure borrowers have the ability to repay their debt regardless of future circumstances: foreseeable or not. So, let’s see how they are doing so far.

5-Star JPMorgan Chase Bank, N.A., Columbus, OH has the largest slice of the multifamily residential real estate pie with about 13.5% of the total amount outstanding, or $80 billion. As of March 31, 2023, none are reported as repossessed; $60 million is 90 days or more past due (or in nonaccrual status). That translates to a delinquency rate on these loans of 0.075%. That is certainly nothing to worry about.

5-Star Flagstar Bank, N.A., Hicksville, NY, is the second largest multifamily lender with about 6.4% of the total (less than half of what JPMorgan has). Flagstar did report $714,000 in repossessed multifamily plus $12.6 million that is 90 days or more delinquent (or nonaccrual) which calculates to a an even lower delinquency rate (0.035%) on its multifamily loans.

Flagstar Bank, if you recall, changed its name at the end of 2022 from New York Community Bank. Then, on March 20, 2023, it acquired Signature Bridge Bank, which was created to resolve the failed Signature Bank. These numbers are reflective of the bank after all of that.

So, we know the biggest multifamily residential real estate lenders are doing quite well. There are another 50 banks where multifamily loans represent at least one-third of total loans reported. They can be found on page 5 of this week's Jumbo Rate News. They too, are in very good financial shape.

In fact, 68% have no multifamily non-performers at all, and most of the others report less than half of a percent. There is one that stands out, however: 4-Star United Orient Bank, New York, NY. At March 31, 2023, United Orient reported that $50.624 million of its $90.674 million total loans is invested in multifamily residential real estate. That’s 55.8% of total loans. Of those, none are 90 days or more delinquent and still accruing, but $1.281 were no longer accruing. That’s over 2.5% and that’s a lot.

United Orient also had $450k in 30-89 days past due multifamily as well as $193k in other commercial real estate that is 30-89 days past due. Its 1.4% total delinquency to loan ratio is high compared to its peers, which reported an aggregate 0.54%. We’ll be watching to see if these past dues devolve into the 90 day+ category when we get its June data. Most others are well below 1%. That’s a good sign.

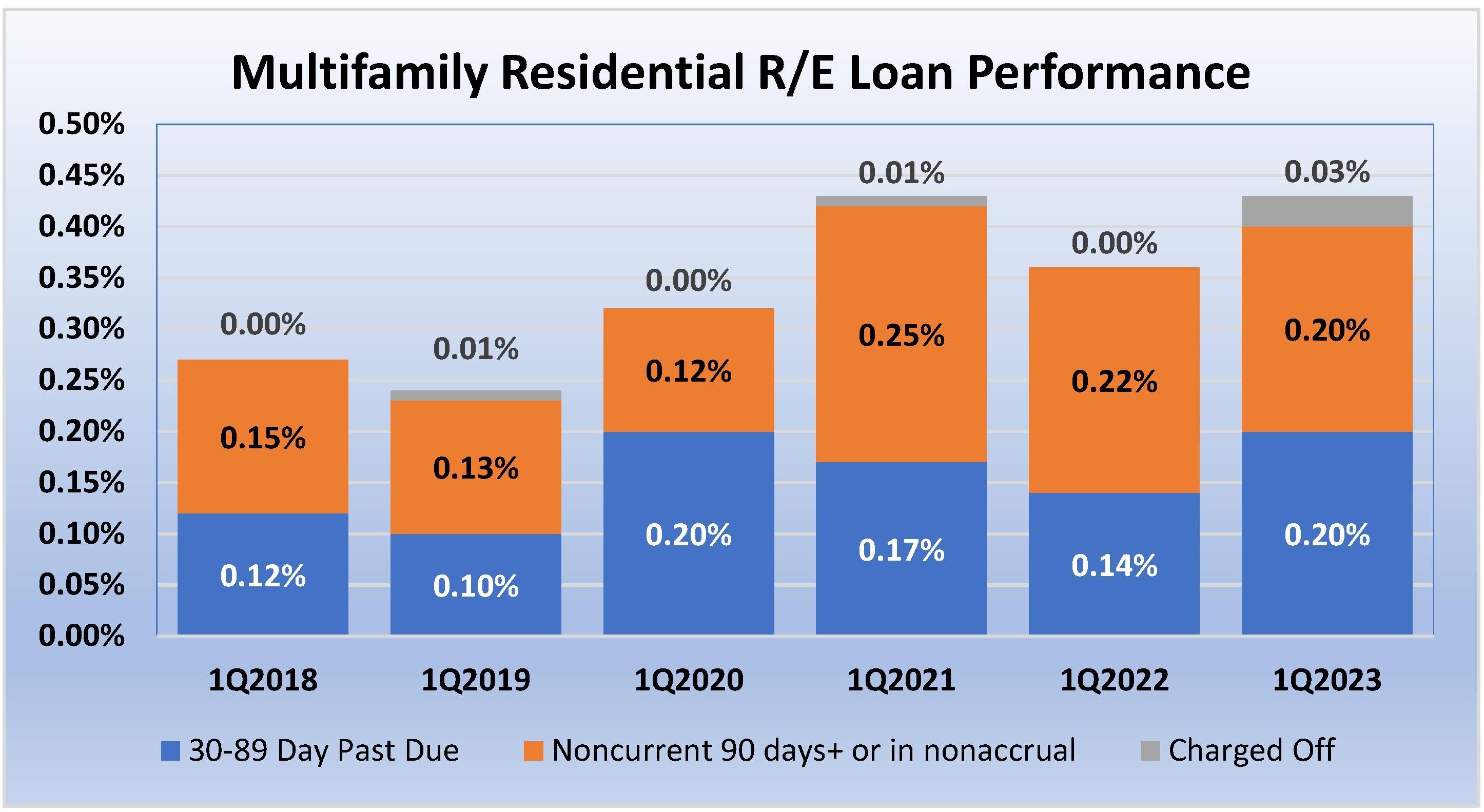

The following chart depicts the five-year progression of non- and under-performing multifamily residential real estate loans at U.S. banks. Before the Covid lockdown, only 0.24% of these loans were in arrears. By March 31st of this year, that percentage was up to 0.43%. That is still not a concerning amount, yet with this amount of growth in just four years, it definitely warrants watching.

Source: FDIC Quarterly Banking Profile