What a difference a year makes, both in attitudes and in numbers. TransUnion®’s Second Quarter 2023 Consumer Pulse Study reports that 57% of Americans are optimistic when it comes to their household finances over the next year. That number, however, varies greatly by age. Only 41% of Baby Boomers feel that way, while the youngest, the Gen Z’ers, report the most optimism at 73%.

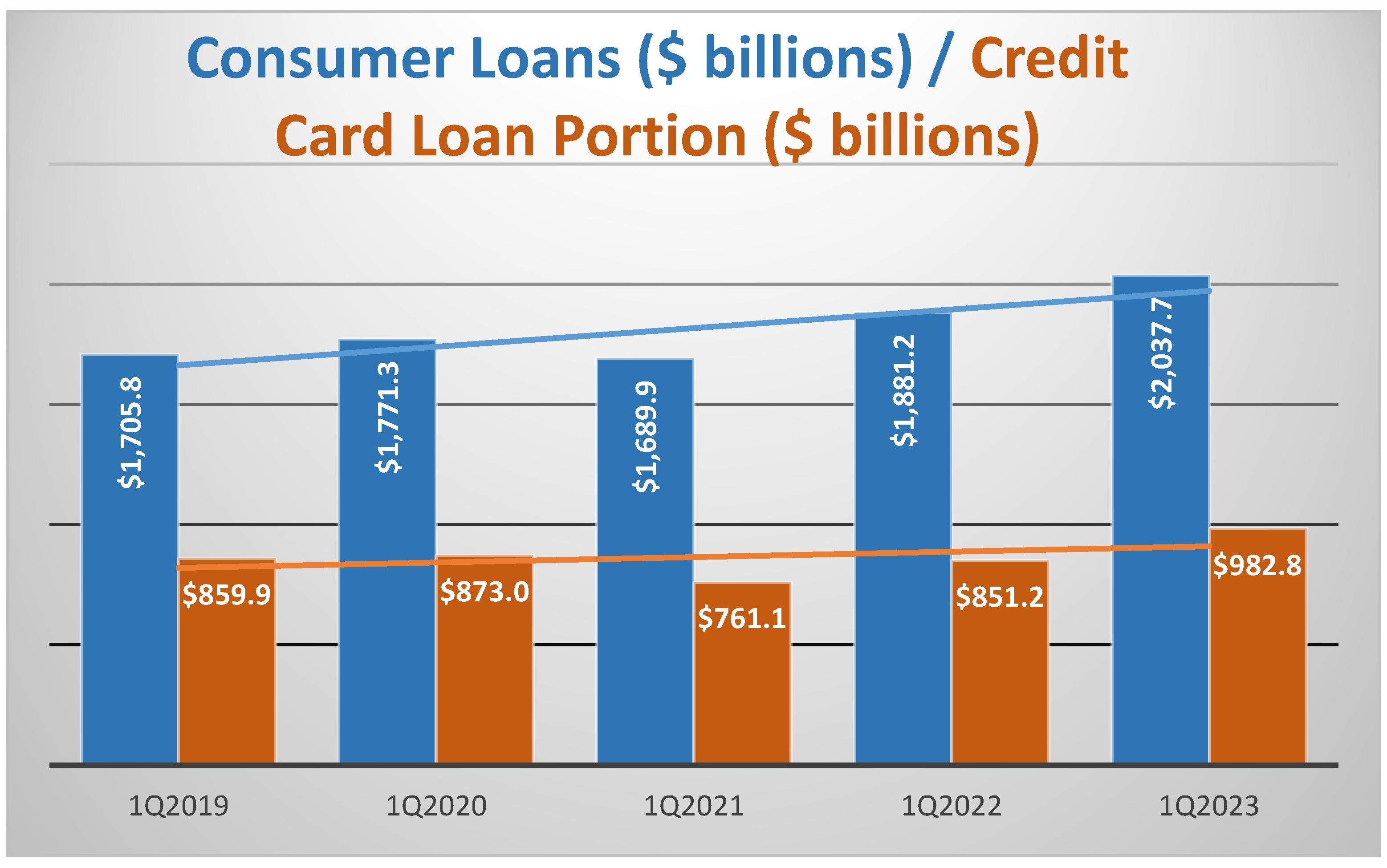

What we are more concerned about, of course, is the numbers. Last year at this time, we were cautiously optimistic about personal credit. Credit card usage was still below pre-pandemic levels, and while total loans to consumers had surpassed 2019 levels, we had hoped to see it subside. It has not:

In fact, even though Americans paid down loans during the pandemic, credit card debt is 14% higher than it was four years ago. Total consumer debt is nearly 20% higher. What’s worse, according TransUnion, is that nearly a third of consumers are planning on increasing that debt even more in the next 12 months. Only 27% of consumers believe their income is keeping up with inflation.

That bears out in the numbers as well. Charge-offs of consumer loans increased from 1.09% a year ago to 1.93% at March 31, 2023. The credit card portion of those loans fared even worse going from 1.85% last March to 3.09% this March 31st.

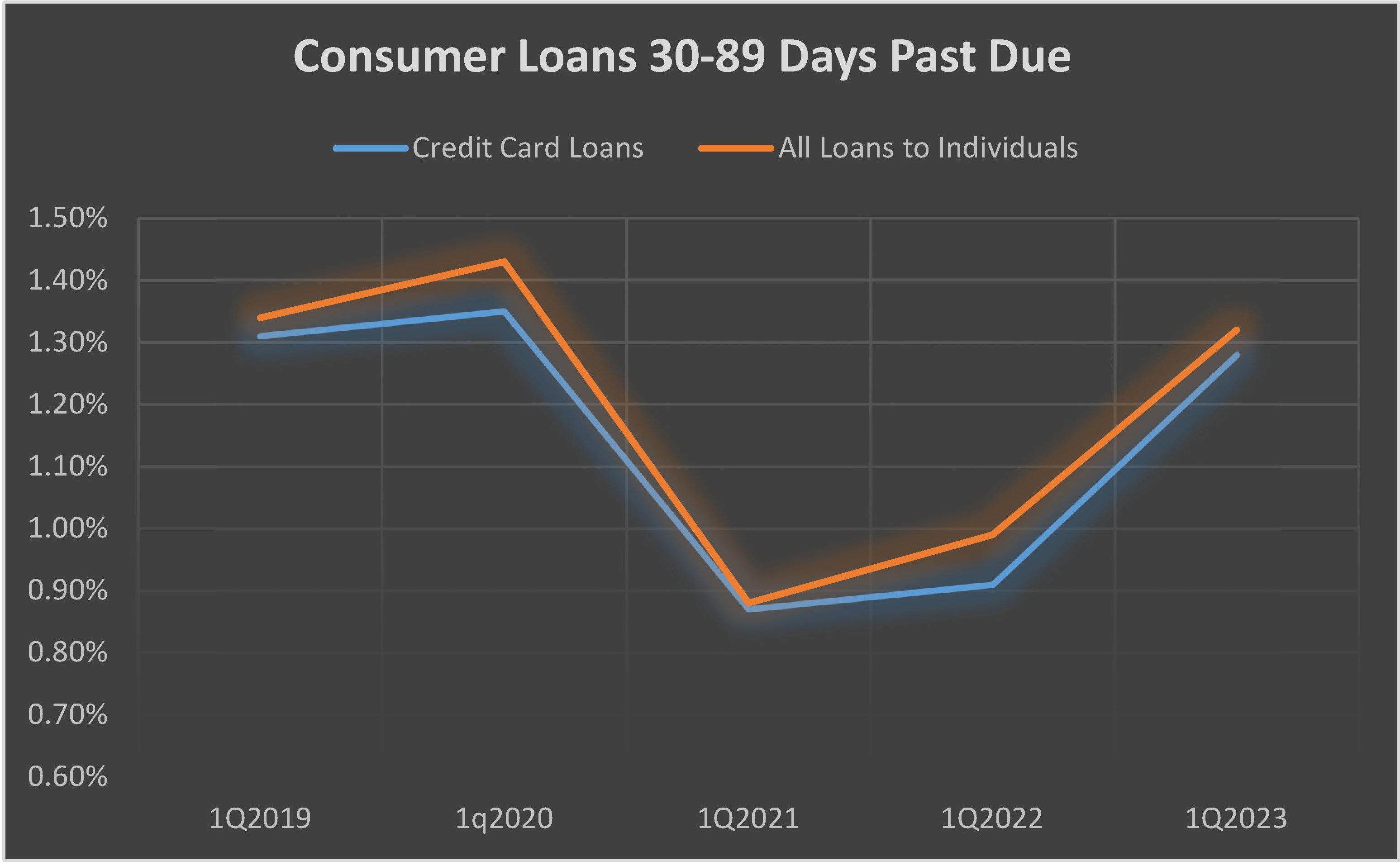

Loans 90 days or more delinquent posted smaller, but still concerning, increases: credit card delinquencies rose from 0.91% to 1.35% and total delinquent loans to individuals rose from 0.66% to 0.91%. Now take a look at the 30-89 day past dues:

They are almost right back up to where they were before the pandemic. Credit cards are 3 basis points lower and total consumer loans are just 2 basis points lower than at March 31, 2019. Both were below 0.9% two years ago (3/31/21).

Not every bank will be affected in the same way if these loans sour, but we do have our eyes on some that may be negatively impacted. On page 5 you will find a list of 51 community banks where loans to consumers constitute more than 10% of total loans. These banks each reported consumer loan growth between March ’22 and March ’23. They also reported higher delinquent consumer loans this year. Lastly, none are rated 5-Stars.

We also looked at 68 banks where delinquent consumer loans exceeded 4% of total consumer loans at March 31, 2023. Only five also reported that at least 20% of their loan portfolio was consumer loans and two of those have barely any loans at all. That leaves the following three; they are not on page 5:

As a bank with a credit card specialization, 3½-Star Merrick Bank, South Jordan, UT’s entire loan portfolio is dedicated to consumer loans, 80% of which is credit card loans. As of March 31, 2023, 5.56% of its loan portfolio is delinquent 90 days or more or in nonaccrual status. An additional 4% is in the pipeline (reported as 30-89 days past due).

With a 4.25% nonperforming assets ratio, Merrick Bank is clearly struggling with loan quality. But, it has very high capital ratios, so even if it were to take a hit on all of its delinquent loans, its capital ratio would still be 16.9%. (It is also a JRN listee.)

Consumer loans constitute 22.1% of 4-Star First National Bank, Killeen, TX’s loan portfolio (or $380.5 million). It has no credit card loans, but 5.1% are 90 days or more delinquent or in nonaccrual status. Another 27% are 30-89 days past due. FNB Texas is a $4.3 billion asset bank, but only $1.7 billion is loans, so while nonperforming loans are high, as a percent of total assets, they are right in line with its peers (0.54% vs. 0.52%).

Similarly, 4-Star Southeast Bank, Farragut, TN has no credit card loans, but 60% of it portfolio is in consumer loans and 6.3% are delinquent 90 days plus.

The bank with the highest delinquency rate on its consumer loans is actually a Fintech. 3½-Star Green Dot Bank, Provo, UT reported that 9.57% of its consumer loans were 90 days or more delinquent (or in nonaccrual status) at the end of Q1. And yes, 70.2% of its loans are consumer loans, but its loan to deposit ratio is only 1%.

Green Dot Bank has a leverage capital ratio (CR) of 8.87%, which is lower than the 10.1% of its peers, but at over 30%, its risk-based CR is more then double that of the peer group. In addition, Green Dot Bank’s delinquency to asset ratio is just 0.07% while that of its peer group is 0.52%. That’s why we have to look at the entire picture.