Let’s face facts. From a bank perspective, core deposits are the best deposits. Core deposits are typically from the local area and from customers who generally have a relationship with the bank that incorporates more than just a savings account or CD. As such, core deposits are considered to be a more stable source of funding than non-core deposits.

As far as non-core deposits, there are two kinds:

- Deposits that come from listing services (like JRN) or advertising (online or off-line), and

- Brokered deposits.

To attract deposits, both types of non-core deposits tend to be more expensive to the bank than core deposits (and also more lucrative for depositors), but brokered deposits incur additional fees. As a result, brokered deposits are the most expensive way to fund growth.

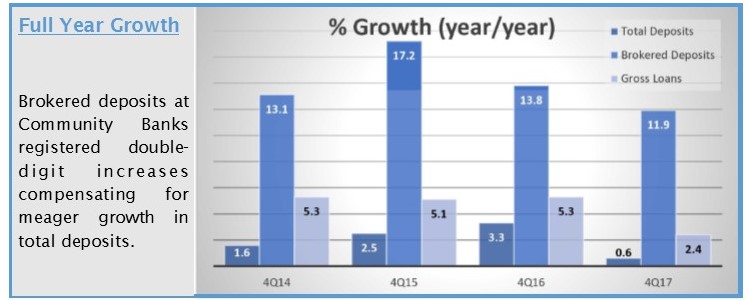

Robust loan growth over the past few years has sent many banks down the brokered path. The chart below indicates clearly how deposit growth was not enough to cover what was needed to fund the 5% plus loan growth. Many banks resorted to high-priced and volatile brokered deposits. Not only is that a very expensive tactic, it could end up backfiring, especially since loan growth was cut in half last year. They’d be better off growing core deposits …or listing with JRN.

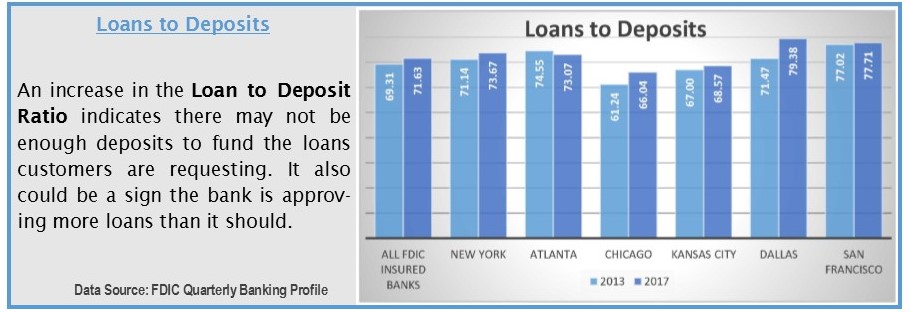

That notwithstanding, there’s another, altogether different reason to be concerned. A high loan to deposit ratio (LTD), according to the Research Department at the Federal Reserve Bank of Philadelphia, may indicate aggressive or risky lending. The report also indicated, however, that small banks in particular, have been supplementing their core deposits with FHLB advances. This is a very cost effective and prudent way to accommodate a higher LTD.

The report went on to say that a higher LTD is not as alarming today as it was in the 1990’s. We would also add that each institution has to be looked at individually to determine if there is cause for concern. And, based on the chart below, banks in the Dallas Region especially, should be scrutinized.

Each bank listed on page 7 increased its brokered deposits by more than 1000% during calendar 2017. Here are just a couple:

5-Star Heartland Bank, Gahanna, OH only has $10 million in brokered deposits as of 12/31/2017; but it only had $6,000 a year earlier. Its brokered deposits are less than 1.3% of total deposits. Its LTD is 91%.

Conversely, JRN listee 5-Star State Bank of India (California)’s brokered deposits represent 14.8% of the total, up from less than one-tenth of 1% a year ago. Brokered deposits at 5-Star MidCountry Bank, Bloomington, MN increased from 1.05% to 16.64% during the year. Both have LTDs exceeding 100%. Fortunately, you don’t have to worry. Bauer has its eye on them.