By now you probably know that the Federal Reserve’s Open Market Committee lowered the Fed Funds target a quarter point on Wednesday (July 31st). The range is now between 2% and 2.25% with another quarter point cut widely expected before the year is done.

The primary reason? Inflation is too low. In spite of the fact that the U.S. economy and labor markets are both doing well, inflation has remained stubbornly below the 2% target rate all year. The 2% target was officially adopted in 2012, during Ben Bernanke’s tenure as Fed Chair, but has been elusive. While inflation did reach the 2% mark in December, it has failed to do so since.

Current Fed Chairman, Jerome Powell, prefers to act now while we have a strong economy. Waiting too long, especially when rates are low to begin with, leaves the Fed very little room to work with.

Low inflation wasn’t the only reason for the cut, though. The world is getting smaller, or at least more interconnected and interdependent. The global economy is playing an increasingly larger role in decision-making here at home.

There had been enough chatter about this rate cut that most JRN listees had already accounted for it, so we don’t see any big adjustments in this issue. Banks are a lot quicker to lower savings and CD rates in response (or in anticipation) to Fed moves than they are to raise them. But that’s no surprise. The opposite is true when it comes to loan rates. It all comes down to margins.

Banks have to make more on their earning assets than they pay on deposits. In theory, the greater the margin, the more profitable the bank will be. In reality, when interest margins are squeezed, banks will look for other sources of income. For some banks this means increased lending. While the margin remains the same, they can boost income by sheer volume. For others, the result is higher fees.

It’s been over ten years since banks have had to accommodate a rate cut. The last one was 75 basis points and that was back in December 2008. In fact, between 2007 and 2008, the Fed Funds rate was adjusted down ten times—from 5.25% all the way to 0.25%. Two quarter point cuts this year should be relatively easy for most banks.

Although business models vary, a loan to deposit ratio of 80% to 90% is generally considered optimal. At this level, the bank is lending sufficiently for its size, but not so much that its ability to meet other obligations would be compromised in the event of a downturn. The community banks listed on page 7 are all lending in this “optimal” range.

Additionally, earning assets at each bank listed are doing what they are supposed to do: earning. And quite well, we might add. Each bank listed on page 7 has a net interest margin of at least 5%. To put that in perspective, the annualized aggregate industry net interest margin at March 31st was 3.42%. Of course that varies by the asset size of the bank as you can see below.

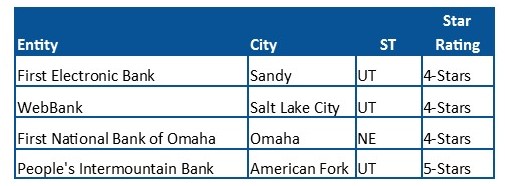

The community banks on page 7 have one more thing in common—they are all recommended by Bauer (rated either 5-Stars or 4-Stars). We don’t expect them to run into any problems with their interest rate spread regardless of what the Federal Reserve does.

To be fair, there are 4 non-community banks that match these criteria as well. They are: