On Friday, August 31, 2018, the NCUA liquidated Zero-Star Melrose Credit Union, Briarwood, NY. We have reported several times in the past on Melrose CU, which was the largest taxi medallion lender in New York, and hence in the country.

The origin of taxi medallions dates back to the 1930s as a means to limit the number of cabs on the streets and allow cab drivers to earn a decent living. These medallions, necessary to drive a cab, were originally available for a meager investment (less than $200 in today’s money). But the supply was limited and this scarcity drove the price up and up. The price peaked in 2013/2014 at over $1 million.

Then along came Lyft and Uber. The price of a medallion is now a fraction of what people bought them for …and what Melrose Credit Union financed them for. Just as people walked away from homes when their mortgages were upside down, cab drivers and medallion investors walked away from their loans.

By March 31, 2017, Melrose C.U. was significantly undercapitalized. Its delinquency to asset ratio was 34% and its hopes for survival for slim. The New York State Department of Financial Services took possession of the credit union on February 10, 2017. The NCUA was named as conservator.

Melrose continued to deteriorate. In April 2017 (JRN 34:14) we wrote that Melrose was “quite literally fighting for its survival”. By April 2018 (JRN 35:15) we surmised “It is highly unlikely it can survive”.

Melrose was not the first to succumb. Zero-star Montauk Credit Union, New York, NY had been in a similar situation but only lasted until March of 2016. And we still have our watchful eyes on two others: Zero-Star LOMTO Federal Credit Union, Woodside (Queens), NY and 2-Star Progressive Credit Union, NY, NY.

LOMTO’s days are surely numbered. It has been critically under-capitalized for over a year and rated Zero-Stars for two years. It’s got one foot in the grave and the other on a banana peel.

Progressive is in a better position with a good capital cushion, but delinquencies are taking their toll.

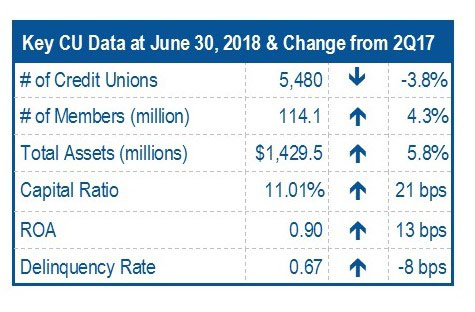

New York City and its taxi medallion mess notwithstanding, second quarter credit union financial results were actually quite positive. See chart for key details.

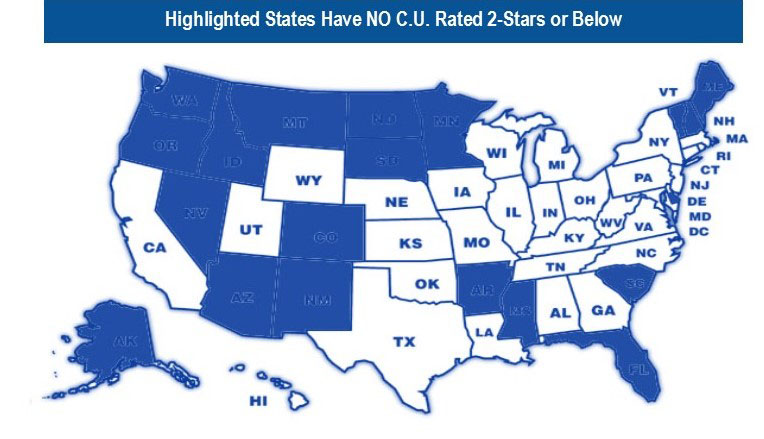

For the first time in six quarters, Bauer’s Troubled and Problematic credit unions (the 136 currently rated 2-Stars or below) represent fewer than 2½% of the industry. Credit Unions rated 5-Stars or 4-Stars, and therefore recommended by Bauer, have surpassed 81%!

At 7.5%, New Jersey has, by far, the highest percent of Troubled and Problematic credit unions, that’s up from 6.0% based on June 30, 2017 data. New York and Connecticut are tied for the second highest percentage at 5.2%. The difference is that New York has actually improved slightly from 5.3% last year. Connecticut has deteriorated from 4% a year ago. Rhode Island rounds out the bottom four at 5%, unchanged from last year. Seventeen states plus Puerto Rico have none—up from 15 a year ago; they are highlighted on the map.

Oregon and Washington each have 96.6% of their credit unions rated 5-Stars or 4-stars making the North Pacific shine bright. Maine follows directly behind at 96.4% and then Florida at 96.3%. Three out of the four improved from last year. Washington was the exception, it held the lead alone at 96.7% a year ago.