You have probably already heard that the Federal Reserve bumped interest rates up a quarter point on Wednesday (3/16/22). You may have also discerned that we are looking at as many as six more boosts this year. Since the Fed’s Open Market Committee (FOMC) only has six more meetings scheduled in 2022, that would indicate at least a quarter point hike at each meeting.

But we have our eyes on James Bullard, President of the Federal Reserve Bank of St. Louis, and a rotating voting member of the FOMC. Bullard was the lone dissenter in this latest vote, believing we should have seen a half point jump instead of a quarter point. That would have brought the Fed Funds target to between 0.5% and 0.75% (instead of 0.25% and 0.5%).

This is not the first time we’ve seen Bullard dissent. In June of 2019 (JRN 36:24) we wrote, “for the first time under his leadership, Powell failed to arrive at a full consensus”. At that time, Bullard was pushing for a quarter point cut. Powell et al decided instead to leave the target Fed Funds rate unchanged (at between 2.25% & 2.5%).

The fact that Bullard wanted to cut rates before the rest of the Fed members is telling as he is considered to be the most “hawkish” member of the FOMC. Hawks, as a rule, tend to want tighter monetary policy (higher rates). He may have just been ahead of the curve. Or, Powell may have wanted to assert his independence from POTUS, as the white house was making it very clear it wanted a rate cut.

In either case, the following three meetings each ended with quarter point cuts. The Fed Funds target then remained unchanged through the following two meetings which spanned a four month period. But then…

The pandemic hit (March 2020) and two emergency meetings later, the Fed Funds rate was brought down a full point and a half, to near zero (between 0% and 0.25%). And that is where it remained, until now.

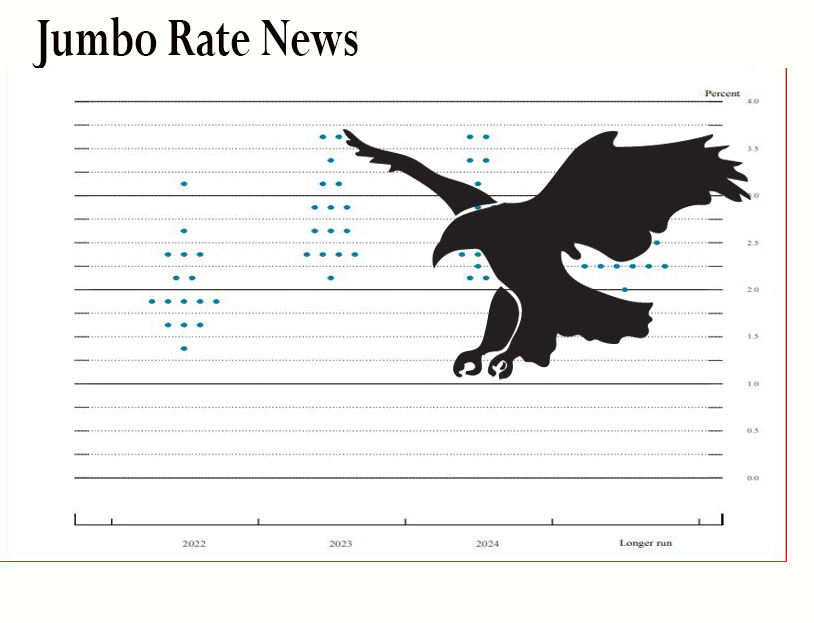

The dot plot, a graphical prediction of where rates will likely end up this year and in coming years, is where Bullard’s hawkishness does stand out. Out of 16 predictions, his is the only one that ends 2022 above 3%.

If we throw out the highest (Bullard’s) and the lowest (between 1.25% and 1.5%), we are still left with a full point spread—from between 1.5%-1.75% all the way up to between 2.5% and 2.75%. All predictions for 2023 are above 2% with two going above 3.5%.

Remember, these are only predictions. They are subject to change as other factors affect the economy. As for us, we would love to see CD rates start earning a higher rate than inflation, but that does not look like it will happen any time soon. In the meantime, banks are bloated with deposits and loan demand, which has been sluggish, is bound to slow even further as rates go up.

This deposit glut will keep CD rates down even as the Fed Funds rate goes up. This is particularly true for the 49 community banks listed on page 7, which all have these commonalities:

- They were all established more than 5 years ago;

- During the year 2021, total Deposits grew by at least 25%;

- They started 2021 with loan to deposit ratio greater than 70%; but

- Ended 2021 with a loan to deposit ratio below 60%.

At the end of 2021, the average net interest margin (NIM) at all US banks dropped to 2.54%, its lowest level in recent history. The majority of the banks on page 7 reported a higher NIM than this average, but are still likely feeling the squeeze.

5-Star First National Bank Alaska, for example, reported a 2.89% NIM at the end of 2021. Yes, above the average, but also well below the 3.46% it reported a year earlier.

That’s nothing compared to 4-Star California First National Bank, which saw its NIM plummet from over 4% a year ago to about 1.25% today. An interesting tidbit about California FNB is its recent and heavy reliance on brokered deposits. At the end of 2020, it had no brokered deposits on its books. By the end of 2021, brokered deposits represented 39% of California First’s total deposits.

Two other banks listed also rely (perhaps a little too much) on brokered deposits: 4-Star CBW Bank, KS (25.8%) and 5-Star State Bank of Reeseville, WI (12%). Brokered deposits are not bad per se, but they can be expensive. Paying a broker, especially in today’s environment, doesn’t make a whole lot of sense. But, in this particular case, CBW Bank’s NIM actually went up during 2021—from 2.14% to 6.06%. So it goes.