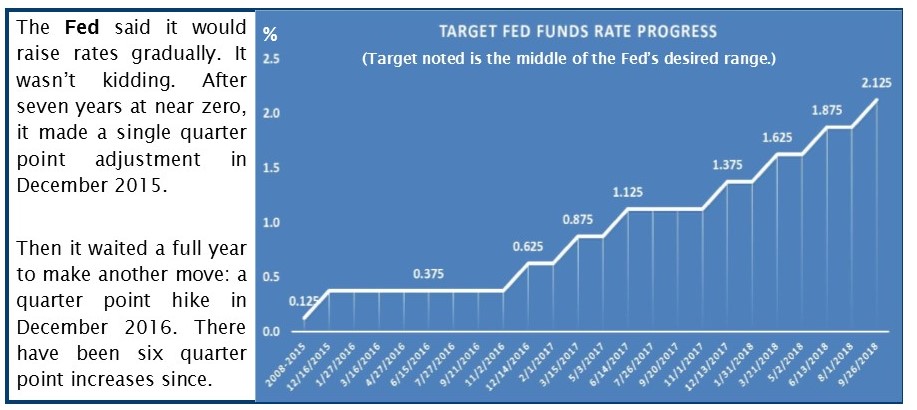

The Federal Reserve raised the target Fed Funds rate another quarter point at its Open Market Committee meeting on Wednesday. As always, banks began raising their lending rates immediately and, as always, CD rates will follow. In fact, they’ve already begun.

The U.S economy marked the beginning of its 10th year of expansion in grand style. Core inflation hit the Fed’s target rate of 2% at the end of August and at 3.9%, unemployment is now at the lowest level we’ve seen in nearly 2 decades.

The Fed Funds target increase was pretty much a foregone conclusion. The quarter percentage point was also presumed. In fact, some Fed officials have been suggesting we will be seeing a lot more of these quarter point bumps in the next year or two. The next one is likely to hit this December.

As CD rates rise, we see more and more banks competing for deposits. In the 12 month period ending June 30, 2018 total domestic deposits at U.S. banks grew by just 3.9%. (Typically that number exceeds 5%.)Conversely, certificates of deposit at U.S. banks grew more than 10%. The previous 12 month period saw a 3½% decline in CDs at U.S. banks.

This heightened interest in CDs just happens to coincide with a proposed rule by the FDIC to exempt certain reciprocal deposits from being considered brokered deposits. The proposal was in response to the Economic Growth, Regulatory Relief, and Consumer Protection Act (S.2155) that was signed into law in May (JRN 35:13, 18, 19 & 23).

The FDIC is proposing that if an institution is both well-capitalized and well-rated, it would not have to report reciprocal deposits as brokered up to certain limit—either $5 billion or 20% of its total liabilities, whichever is less.

Not only will this have the potential to lower deposit premiums paid by these banks, it may also further drive up competition for CDs. And that’s good news for us. Higher rates and more banks in the market!

Comments on the proposed rule will be accepted for 30 days after publication in the Federal Register.

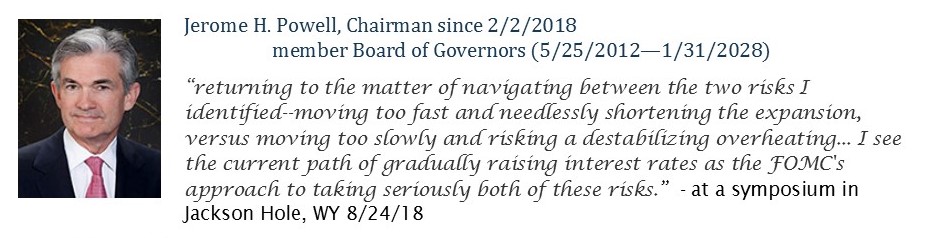

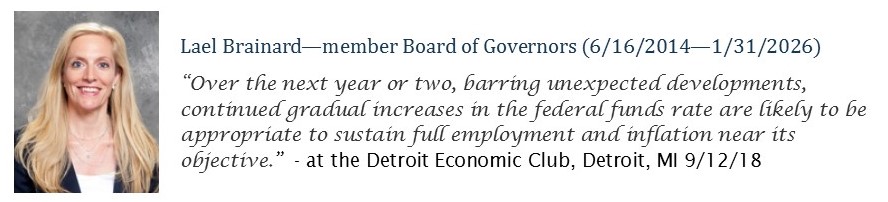

What Fed Officials Say About Rates Heading Up: