According to the FDIC’s Quarterly Banking Profile (QBP) for June 30, 2018, bank industry loans to consumers increased nearly five and half percent from June 30, 2017 to June 30, 2018. Credit card loans, a subset of those consumer loans, increased 7.4% during the same time frame. For the most part, consumers are managing credit card debt well.

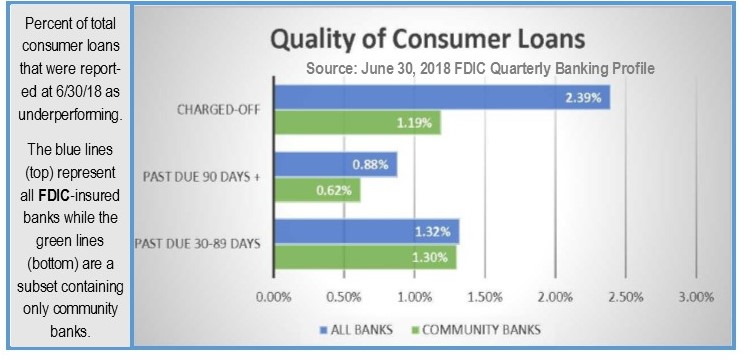

In fact, according to the QBP, consumers are handling most of their bank debt judiciously. And, if you look at the graph (below) you’ll see that consumers who use community banks instead of BIG banks are doing the best.

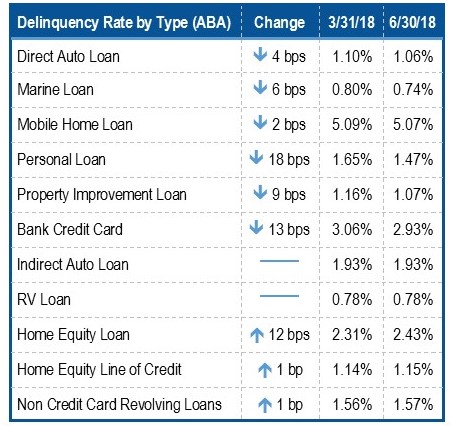

On Thursday (10/4/2018), the American Bankers Association (ABA) released its own report on its consumer delinquency rate survey. The ABA report has a more detailed breakdown on loan types but does not have the benefit of breaking down community banks from other banks. That has been left to us, and combing the two reports, we found some very telling data.

The ABA defines delinquent as 30 days or more past due. The FDIC Quarterly Banking Profile (QBP) breaks delinquencies down farther (as pictured below). We can clearly see that from 30-89 days past due, community banks don’t hold much of an edge over the industry as a whole (just 2 basis points—1.30% vs. 1.32%). But that changes as we get to more serious delinquencies. Loans delinquent 90 days or more represent just 0.62% of consumer loans at community banks but account for 0.88% of the industry. And, at 1.19%, consumer loan charge-offs at community banks are 120 basis points (or 1.2 percentage points) lower than the banking industry as a whole. That’s great news, but in a tribute to the late Paul Harvey, here’s “The Rest of the Story”.

While most loan categories showed improvement in delinquency rates this quarter, home equity loans faltered. According to the ABA, delinquency rates for both home equity loans and home equity lines of credit (HELOCs) were both up. While they remain well below their respective 15-year averages of 3.00% and 1.21%, delinquent home equity loans were up 12 basis points during the second quarter while HELOCs were up one basis point.

Now we turn back to the QBP to find that the primary blame for these rising delinquencies does NOT lie with community banks, but with credit card banks. There are currently only 12 banks labeled with this specialization, and you know them. These banks include: Chase Bank USA; Capital One; American Express NB; Discover Bank; Synchrony Bank and seven others. According to the QBP, home equity loans 90 days or more past due at ALL FDIC-insured banks represent 2.38% of the total. Banks that specialize in consumer lending have a delinquency rate of just 1.65%. Credit card banks, on the other hand, have a whopping 48.19%! And that’s not all, the charge-off rate for these loans at all U.S. banks at 6/30 was just 0.07%; at credit card banks it was 83.73%. (Talk about skewing a bell curve.) So, render therefore unto credit card banks your Jumbo CDs (as they usually have good rates), but think twice when taking out a home equity loan.